Author

Ruby Wincele | Policy & Research Manager

Contributors

Jordan Gerow ǀ Policy & Research Director

Jacqueline Adams ǀ Senior Policy & Research Associate

Kristen Soares ǀ State Climate Policy Network Manager

The United States is seeing record buildout of data centers, in large part due to the AI boom and generous tax incentives across states. These facilities pose unprecedented risks to our water resources, climate and clean energy targets, energy affordability, and economic outcomes, and their rapid increase poses an even greater risk for the future health and wellbeing of communities.

Data centers are the leading driver of electric load growth, with estimates suggesting demand could reach 106 gigawatts (GW) by 2035. Electricity used for commercial computing is projected to increase faster than any other source in buildings, rising from 8% of commercial sector electricity use in 2024 to 20% by 2050.

This growth is driven increasingly by larger project proposals — projects like the $10 billion, 2,200-acre Meta data center in Louisiana; $165 billion, 3 million square-foot Project Jupiter data center in New Mexico; 1.8 GW, 600 acre Project Jade campus in Wyoming; and the 4.4 GW, 3,200-acre Homer City data center campus in Pennsylvania. Each of these hyperscale data centers represent the equivalent energy demands of a medium-sized city, and the largest of them would rival even New York City’s annual electric consumption.

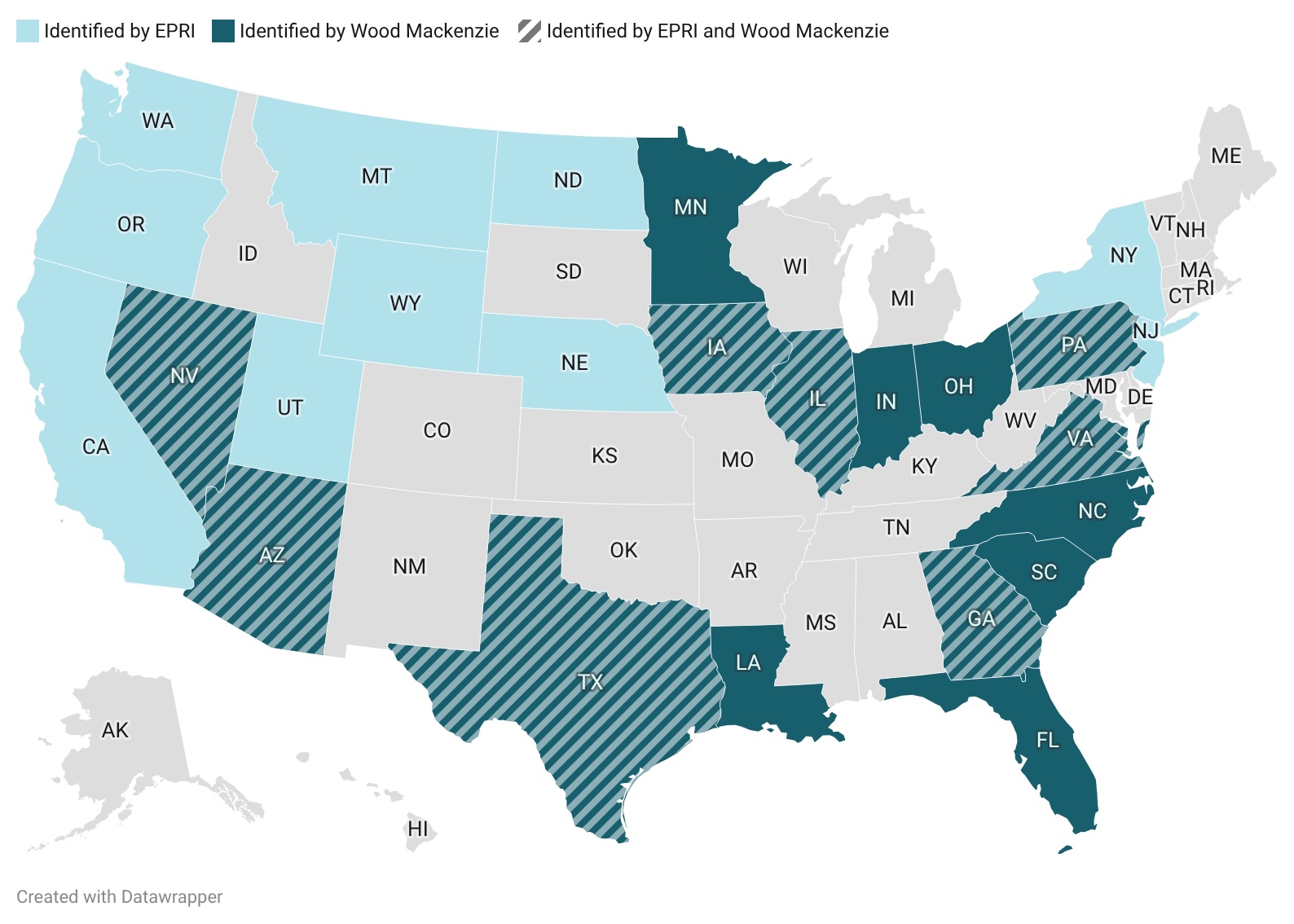

Identifying the states most susceptible to data center impacts is a key first step in implementing guardrails around the rapid development of this industry. In 2025, the Climate XChange team catalogued over 150 different bills, with most aiming to mitigate impacts from data centers, and conducted a 50-state analysis of potential impacts relating to greenhouse gas emissions; the security, stability, and affordability of energy systems; water stress; and state budgets and employment. We identified states most susceptible to each impact, considering the unique energy, water, and economic characteristics of each state.

This article summarizes the key findings of the analysis, and points to opportunities for data center regulation in 2026 and beyond. Later this year, Climate XChange will be releasing five policy toolkits describing the unique levers that state actors can pull to impact outcomes in each of these issue areas, from large load tariffs to water efficiency standards. Finally, we look forward to directly engaging state advocates and policymakers with educational programming and technical assistance on how to use the state data center policy toolkits effectively.

Estimating Data Center Growth Across States

While it’s difficult to pinpoint the exact scale, location, and number of data centers that will actualize — lacking transparency requirements, data center developers have no mandate to disclose information around planned development — this analysis is largely dependent on a combination of two sources that identify current and projected data center development:

- A 2024 EPRI analysis provides two different state datasets on existing data centers: (1) total data center demand in megawatt-hours (MWh) in 2023 by state, and (2) data center energy usage as a percent of total state electricity consumption in 2023

- A 2025 Wood Mackenzie analysis tracks proposed data center projects since 2023, ranking the top 15 states in the country by megawatts (MW). CXC used this to identify states where the buildout of data centers is expected to be highest, based on demand, and we refer to them as “high-growth data center states” in this analysis.

While we are aware that there is great uncertainty in terms of what proposed projects will ultimately become operational, for purposes of identifying priority jurisdictions, we used these two sources to understand the current data center market, and what to expect in the future. Collectively, there are 25 states with the most current and expected data center buildout (referred to in the article as “data center states”).

Map 1. 25 “Data Center States” Identified by Climate XChange

Greenhouse Gas Emissions

Data center proliferation threatens states’ climate and clean energy targets, especially as utility regulators across the country are approving substantial fossil fuel buildout. CXC tracked specific fossil fuel expansions and extensions in eleven states totaling at least 8.5 GW in 2025, and all were tied to data center projects.

Nationally, we’re seeing the largest data center buildout in states that have not enacted many climate policies. It’s important to note that existing climate policy (or lack thereof) does not seem to be a driving force behind data center siting decisions; factors like proximity to necessary infrastructure, geography and climate, power reliability, and tax incentives are driving these decisions. However, buildout in states that lack clean energy targets is a concerning trend when considering data centers’ impacts on air quality and emissions.

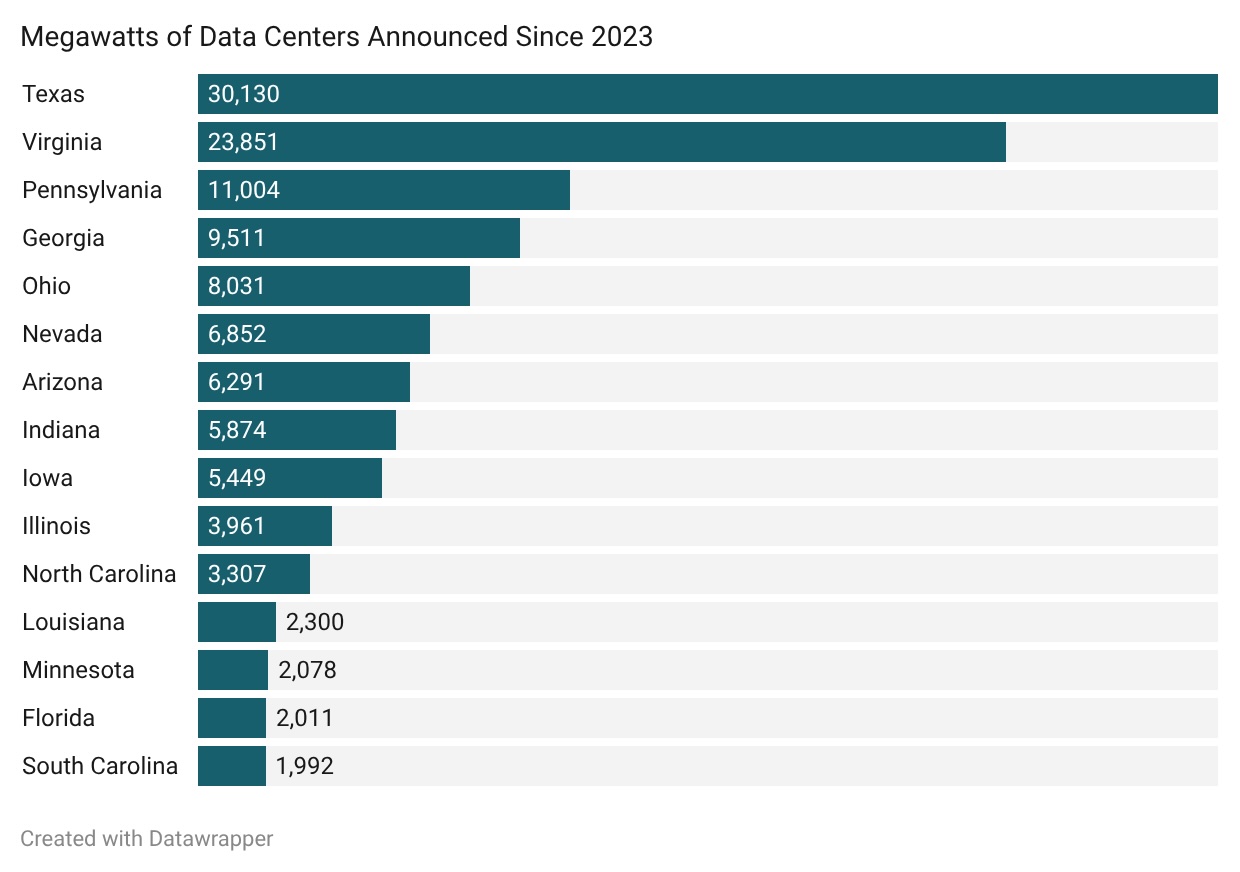

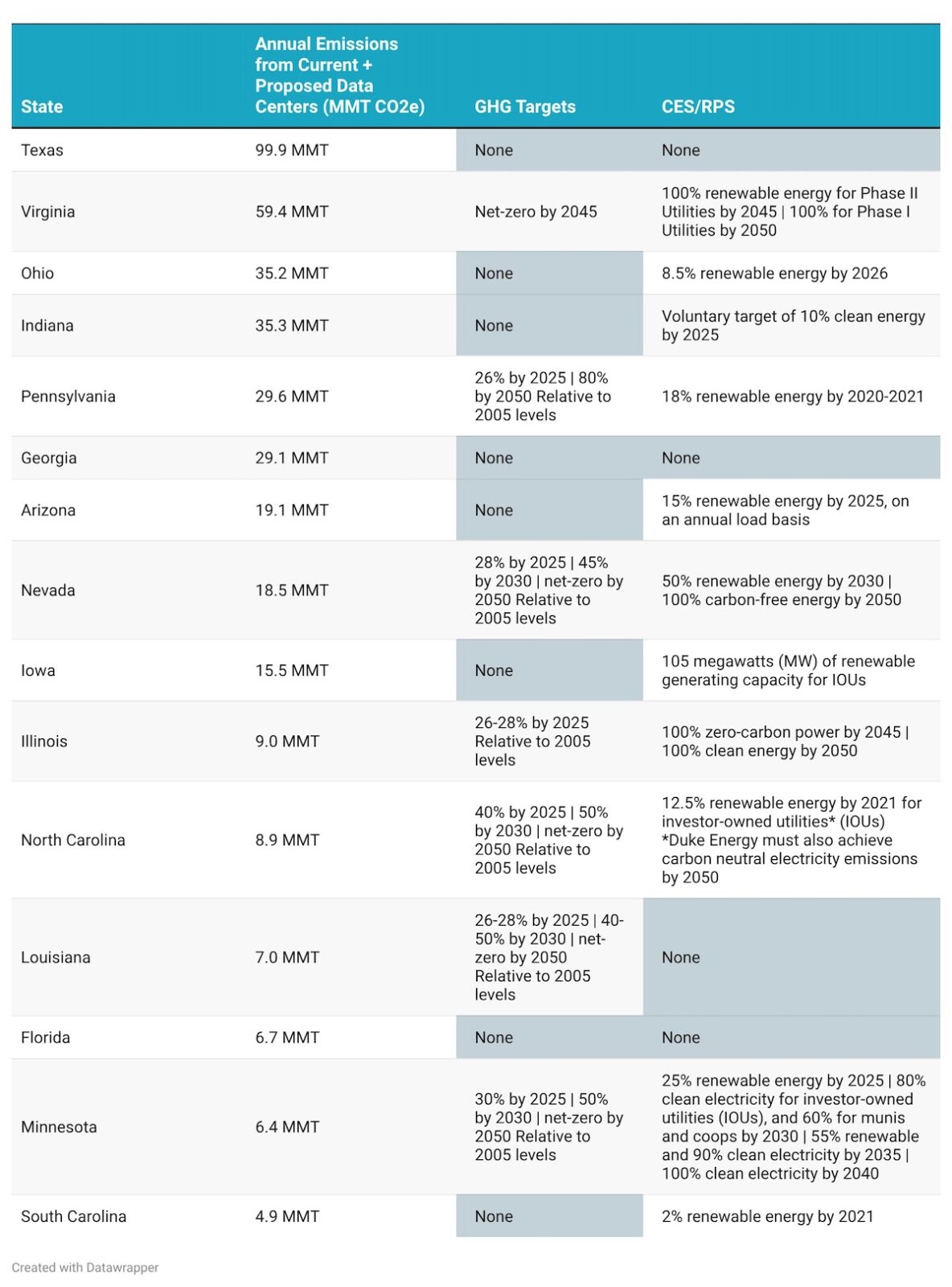

Within the top 15 “high-growth data center states” identified by Wood Mackenzie, 11 have a clean energy standard (CES) or renewable portfolio standard (RPS), but the majority of those standards set minimal clean energy targets and/or don’t extend beyond 2026. Only four of the 15 states have ‘forward looking’ clean energy targets: Virginia, Nevada, Illinois, and Minnesota all require 100 percent clean energy by 2050 or sooner, However, data center proliferation threatens these targets and the Southeast, a region where many states lack clean energy targets, is experiencing a data center boom.

Figure 1. “High-Growth Data Center States” Future Buildout, According to Wood Mackenzie

In the same vein, just about half of these 15 states have greenhouse gas (GHG) emissions reduction targets, with the most ambitious requiring net-zero emissions by 2045 or 2050.

Only three of these states — Virginia, Minnesota, and Nevada — have codified their GHG limits, and, as with clean energy targets, data center proliferation challenges their ability to meet them. In Virginia, for example, assuming all projects proposed between 2023 and 2025 are built and the state’s electricity mix stays the same, annual emissions may reach 59.4 million metric tons (MMT) from data centers alone. This represents nearly 45 percent of Virginia’s gross emissions in 2021 — a staggering figure for a state that must reach net-zero emissions by 2045.

Table 2, below, summarizes these targets, as well as CXC’s analysis of the potential emissions attributable to data centers in states with high expected data center buildout. Our analysis combined present (EPRI) and potential future (Wood Mackenzie) data center load, and estimated the emissions attributable to serving that load, given each state’s electricity emissions intensity.

Table 1. “High-Growth Data Center States” by Projected Emissions, GHG Targets, and Clean Energy Targets

For more information on how these emissions estimates were calculated, please see the methodology.

States that aren’t identified as being among the “top 15” for data center growth and emissions could still see an increase in emissions from data centers. For example, Michigan’s 100% clean electricity law contains an “off ramp” provision that allows utilities to keep fossil fuel generation online if there’s not enough capacity to meet demand, and the Union of Concerned Scientists (UCS) estimates that electric utility emissions will rise by 26 percent between 2023 and 2050 if that loophole is not closed. In Wisconsin, UCS estimates that powering data centers with fossil fuels could result in more than 41 million tons of carbon dioxide emissions between 2026 and 2035, and more than 130 million tons from 2026 to 2050.

Fossil fuel development in high data center growth states

The main reason data center buildout is threatening states’ climate goals is because these facilities are increasingly relying on electricity generated by fossil fuels. This is a two pronged issue: existing, dirty plants are staying online, even past their planned retirement date, and new gas plants are being proposed by utilities to account for growing data center demand.

States are delaying retirement of old fossil fuel plants and also relying on older, more expensive peaker plants as demand spikes. According to the Frontier Group, utilities have delayed the retirements of more than 30 generating units at 15 coal plants across the country over the past two years to provide power to data centers.

If the grid responds to surging data center demand with more output from existing fossil generators instead of new, clean resources, Rhodium predicts this trend could impact U.S. emissions in the coming year or two. Additionally, a Reuters analysis shows that about 60 percent of oil, gas, and coal power plants slated for retirement in the PJM region postponed or canceled those plans in 2025 as a result of increased demand, with most of those being peaker units.

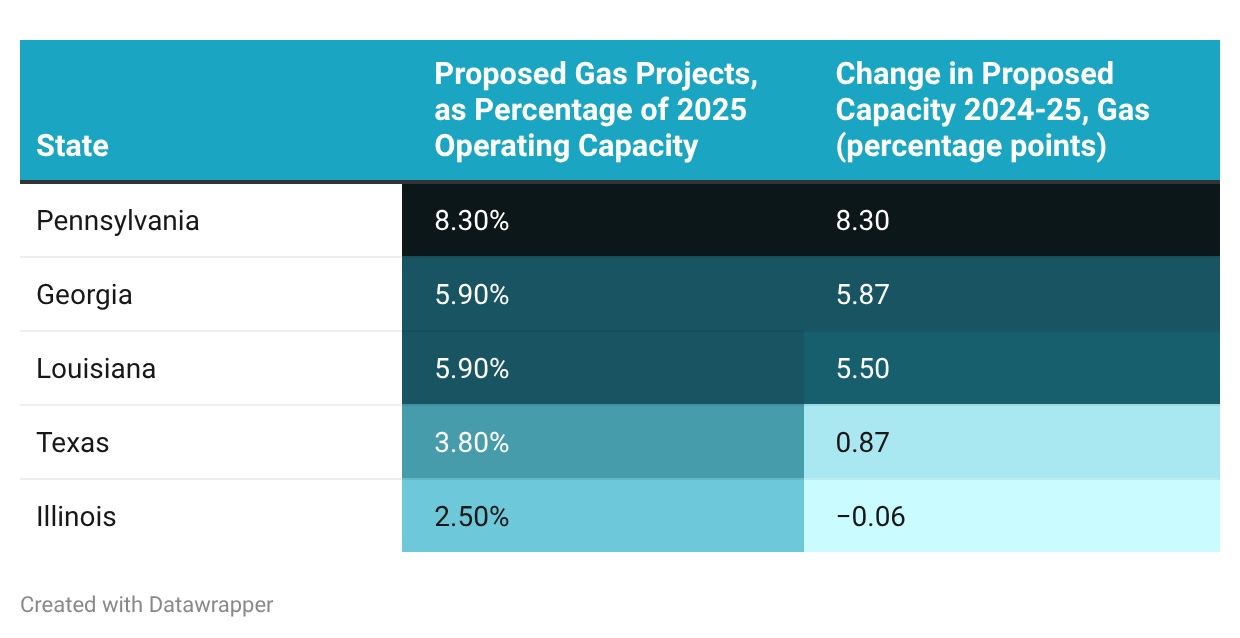

The mix of fossil fuel and renewable energy sources in each state could substantially shift the climate impact of data center energy consumption. CXC looked at U.S. Energy Information Agency (EIA) datasets on proposed power generation to identify the states with the highest proposed gas and renewable energy capacity, as a percentage of that state’s total electric operating capacity in June 2025. We also identified any states that saw an increase in proposed gas or renewable capacity between June 2024 and June 2025, though this analysis didn’t show any clear trends.

Five “high-growth data center states” had new gas proposals in 2025. Of those states, Pennsylvania, Louisiana, and Georgia saw new gas proposals equal to more than five percent of existing capacity. Among states with particularly high amounts of proposed fossil fuel generation, a handful showed an increase in new proposed gas plants between June 2024 and June 2025, indicating that rising data center demand may be occurring alongside increased fossil fuel development activity.

Table 2. Proposed and Change in Natural Gas Capacity in “High-Growth Data Center States”

Renewable energy development in “high-growth data center states”

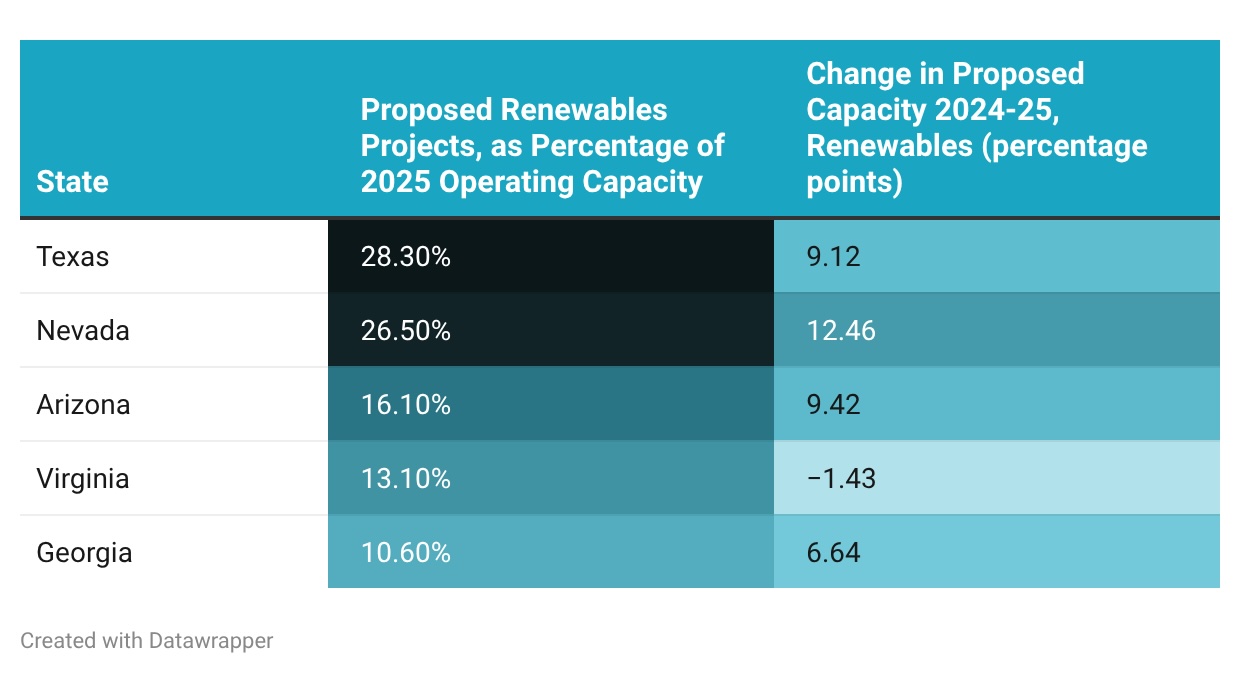

Fortunately, many states are considering renewable energy buildout as well. According to recent EIA projections, utility-scale solar generation will almost double in the next two years. Analyzing EIA generator data, significantly more states have new renewable projects under consideration than new gas projects. In the 15 states where proposed renewables are the highest relative to operating capacity, these proposals range from 10 to 42 percent of operating capacity. Of those states, Texas, Nevada, Virginia, Arizona, and Georgia are all expected to see high data center buildout.

Similarly, 33 states saw an increase in proposed renewable projects between June 2024 and June 2025. Of those states, 19 have been identified as a “data center state” by CXC. This highlights the potential to meet rising demand with a surge in renewable energy in particularly “high-growth data center states”, though it is not a guarantee without guardrails in place.

Table 3. Proposed and Change in Renewable Capacity in “High-Growth Data Center States”

Impacts of data center operations on local air quality

Our analysis didn’t look at how local air quality is impacted by data center growth, particularly as grid operators and data centers embrace the “bring your own power” philosophy that can sidestep state regulations and clean energy targets. A controversial project in New Mexico proposed two gas-powered microgrids that are just shy of the state’s threshold for nitrogen oxide (NOx) emissions, which require more stringent monitoring.

Most data centers also use fossil fuel generators for backup power. These are typically diesel-powered generators that have higher emission rates and emit toxic air pollutants that are harmful to public health. Research estimates that existing backup generators in Virginia could cause 14,000 asthma symptom cases and a total public health burden of $220-300 million per year, impacting residents in surrounding states and as far as Florida. In Memphis, Tennessee, an xAI data center reliant on gas generators, is one of the county’s largest NOx emitters, relying on a loophole in federal regulations to avoid obtaining air quality permits for the turbines.

Policy considerations for addressing data center air emissions

Without explicit requirements for data centers to bring their own clean power, there runs a risk of overreliance on gas and diesel on-site generation and a buildout of new gas plants. States may benefit from studying or regulating data center fuel sources and emissions, including by establishing green power purchase requirements aligned with clean and renewable energy standards, energy efficiency requirements, and co-siting clean energy. Minnesota, for example, enacted legislation last year that explicitly states that the electricity powering data centers achieves every benchmark required under the state’s clean energy standard of 100% clean electricity by 2040, without requesting delays.

Energy Affordability

While there’s not one sole cause of rising energy prices, in general, factors that impact energy affordability are being exacerbated by data centers. Rising energy demand, extending dirty power plants’ lifetimes, relying on costly peaker plants, building new fossil fuel power plants, and investing in grid upgrades to power data centers can all contribute to rising electricity costs.

New Jersey, which ranks 12th for highest existing data center load, has some of the highest electricity prices in the country, and further buildout could exacerbate price increases. In Illinois, a top data center state, the Citizens Utility Board estimated electric bills in the Chicago area could rise as much as $70 in the next three years because of surging demand from the centers.

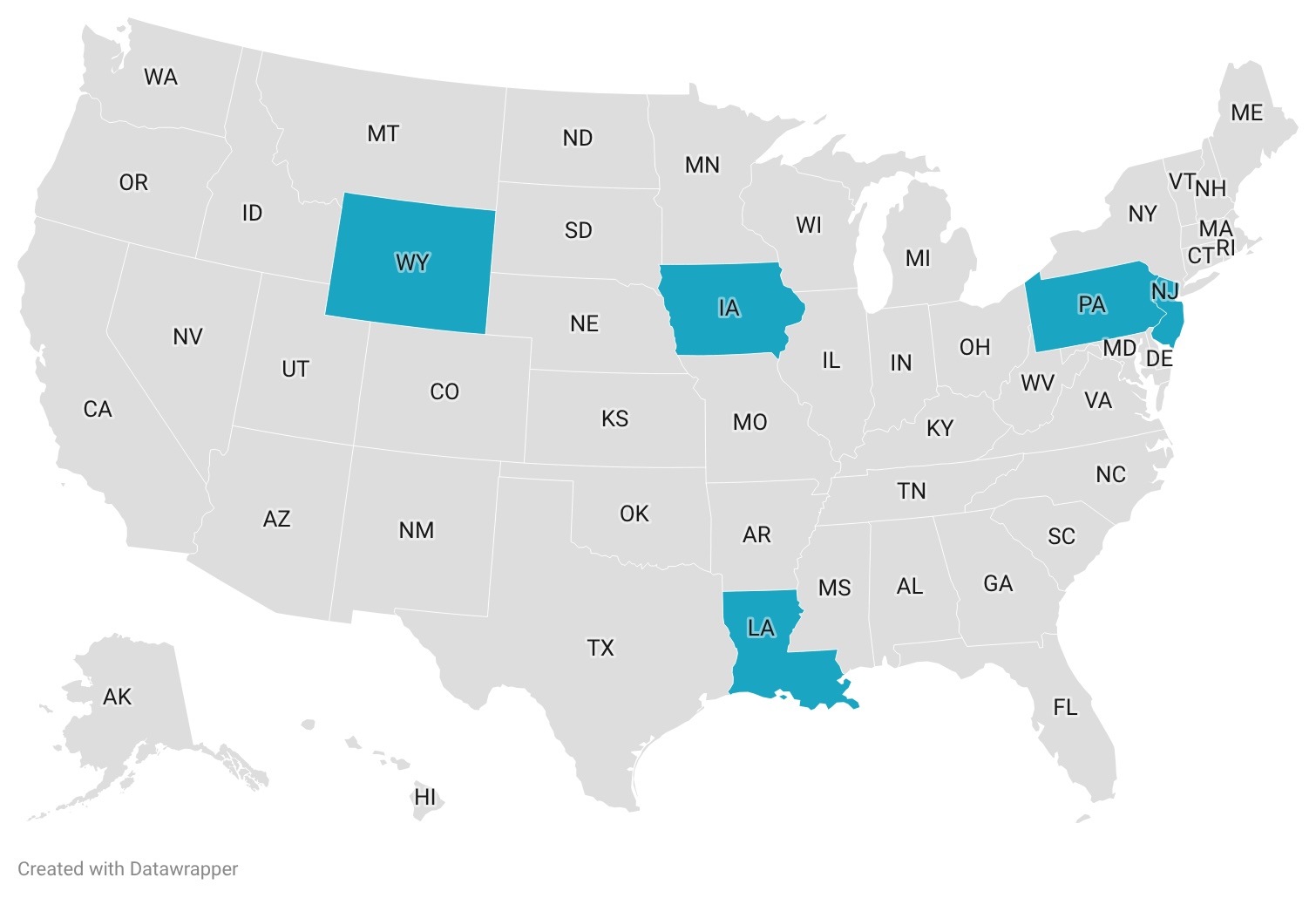

High energy prices on their own might tell one story, but looking at energy burden, or the share of household income spent on energy costs, is an important lens when considering energy affordability. Wyoming, a state where 2023 data center load was ranked 6th in the country for share of electricity consumed, has some of the lowest electricity prices in the country. However, when prices are compared to median household income per capita, the state’s energy burden is one of the highest in the country. We also identified Pennsylvania, Iowa, New Jersey, and Louisiana, each identified as a “data center state” by CXC, and each at risk for exacerbating energy affordability concerns due to their existing energy costs or burdens

Map 2. States Posing Energy Affordability Concerns

Policy considerations for addressing data center impacts on energy affordability

Data center-energy affordability is an area where we saw the most movement across states in 2025. Last year, at least nine states either ordered their utility regulator to establish a new class for “large load” customers, or established a large load tariff for data centers in at least one utility service territory. One estimate found that there are 65 large load tariffs in place or under consideration across 34 states. These large load tariffs are designed to protect ratepayers and shift costs, like increased cost of electricity generation, distribution, and transmission, back to data centers.

However, there’s broad consensus that the steps taken so far do not have strong enough protections for ratepayers. In addition to stronger ratepayer protections through large load tariff proceedings, data centers can also be required to contribute to bill assistance programs. Energy affordability should be examined alongside other issues related to data centers, such as fossil fuel reliance and local air quality concerns, as air pollution exposure falls disproportionately on communities of color and low-income communities.

Energy Reliability

Rising data center load growth can also contribute to grid reliability issues, as high energy use coupled with existing grid unreliability may increase the probability that data center demand will contribute to outages.

To identify states with the most significant reliability issues, we looked at 2023 and 2024 System Average Interruption Duration Index (SAIDI) values, which measure the total time in minutes that an average customer experiences a power outage over one year, factoring in outages due to extreme weather in addition to strain on the grid. Overall, the length of grid outages across all states increased 40 percent between the two years.

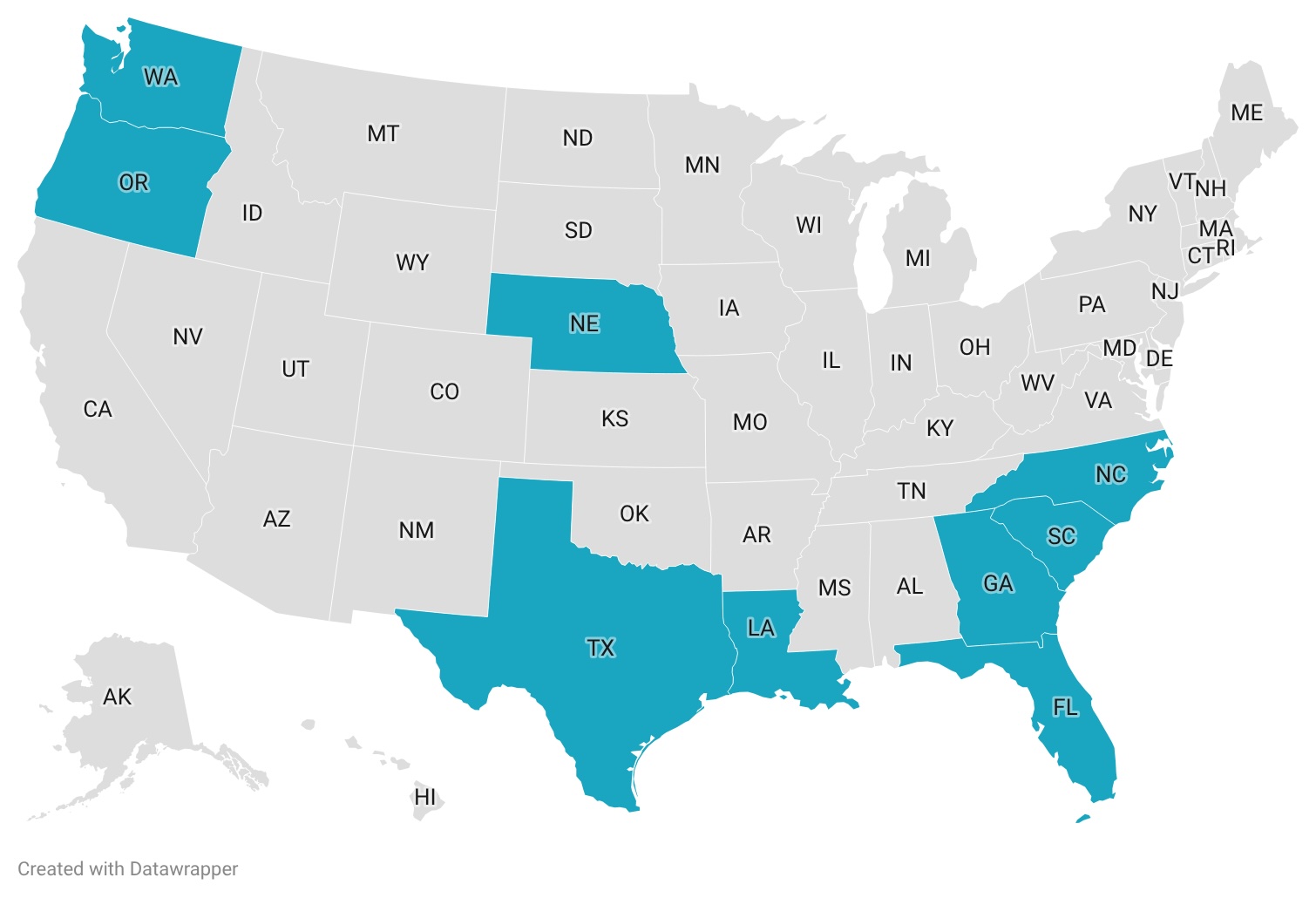

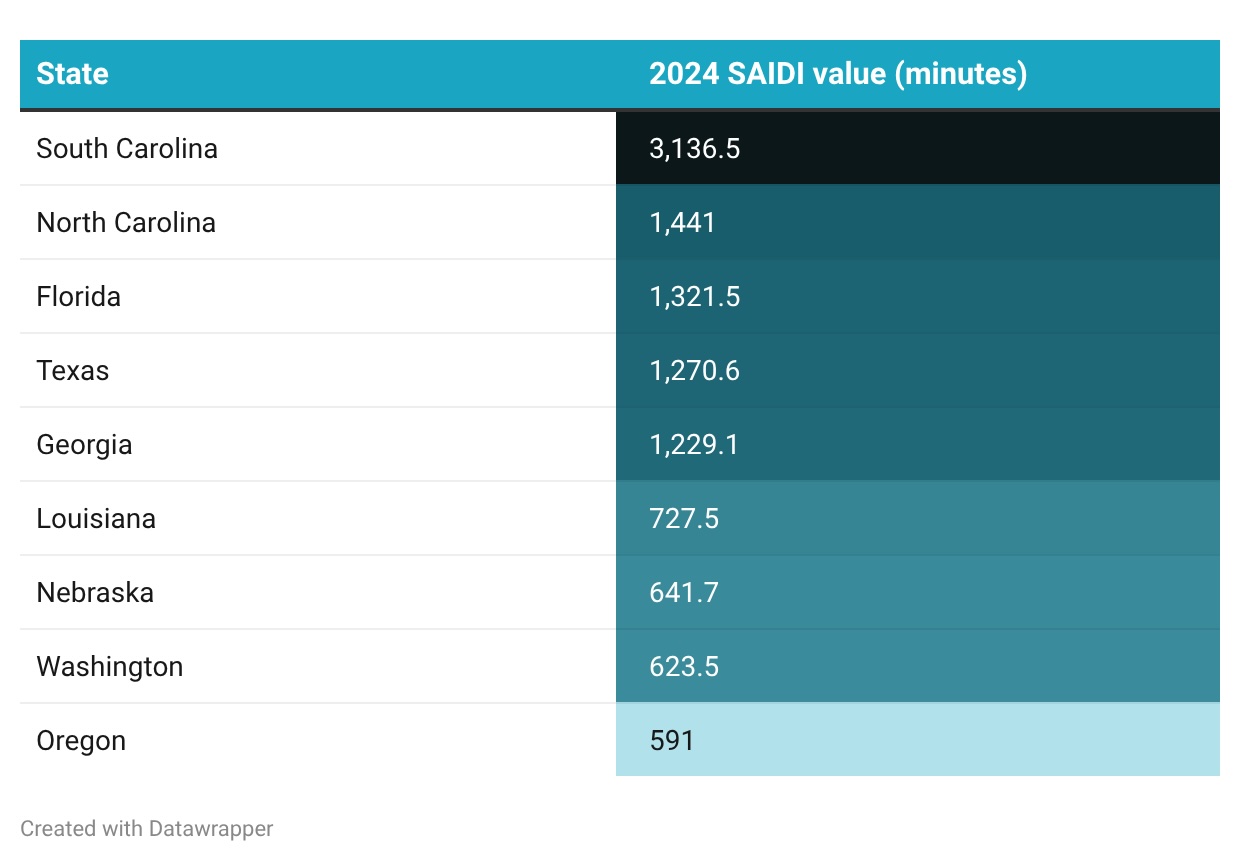

Based on SAIDI data, we found that data centers are being built and proposed in states with already unreliable grids, especially in the face of increased extreme weather events, which risks further strain. Our results showed high SAIDI values in nine “data center states”: South Carolina, North Carolina, Florida, Texas, Georgia, Louisiana, Nebraska, Washington, and Oregon.

Map 3. States with High Vulnerability to Grid Reliability

Table 4. 2024 SAIDI Values for “Data Center States”

Policy considerations for addressing data center impacts on grid reliability

Studies to understand the impacts of data center development on grid reliability is a first step states can take. In states where grid reliability is a particular concern, policymakers may be interested in regulating data center operations to support the electric grid, such as requiring or incentivizing demand response, grid enhancing technologies, and voltage or frequency regulation.

Water Security

Data centers require an extraordinary amount of water to cool their operations and prevent damage to hardware. Large data centers can directly consume up to 5 million gallons per day, equivalent to about 1.8 billion gallons annually, and it’s projected that data center campuses may withdraw as much as 150 billion gallons of water across the country over the next five years. This volume is equivalent to the annual water withdrawals of 4.6 million U.S. households. At the same time, about two-thirds of data centers built since 2022 are in areas with existing high levels of water stress.

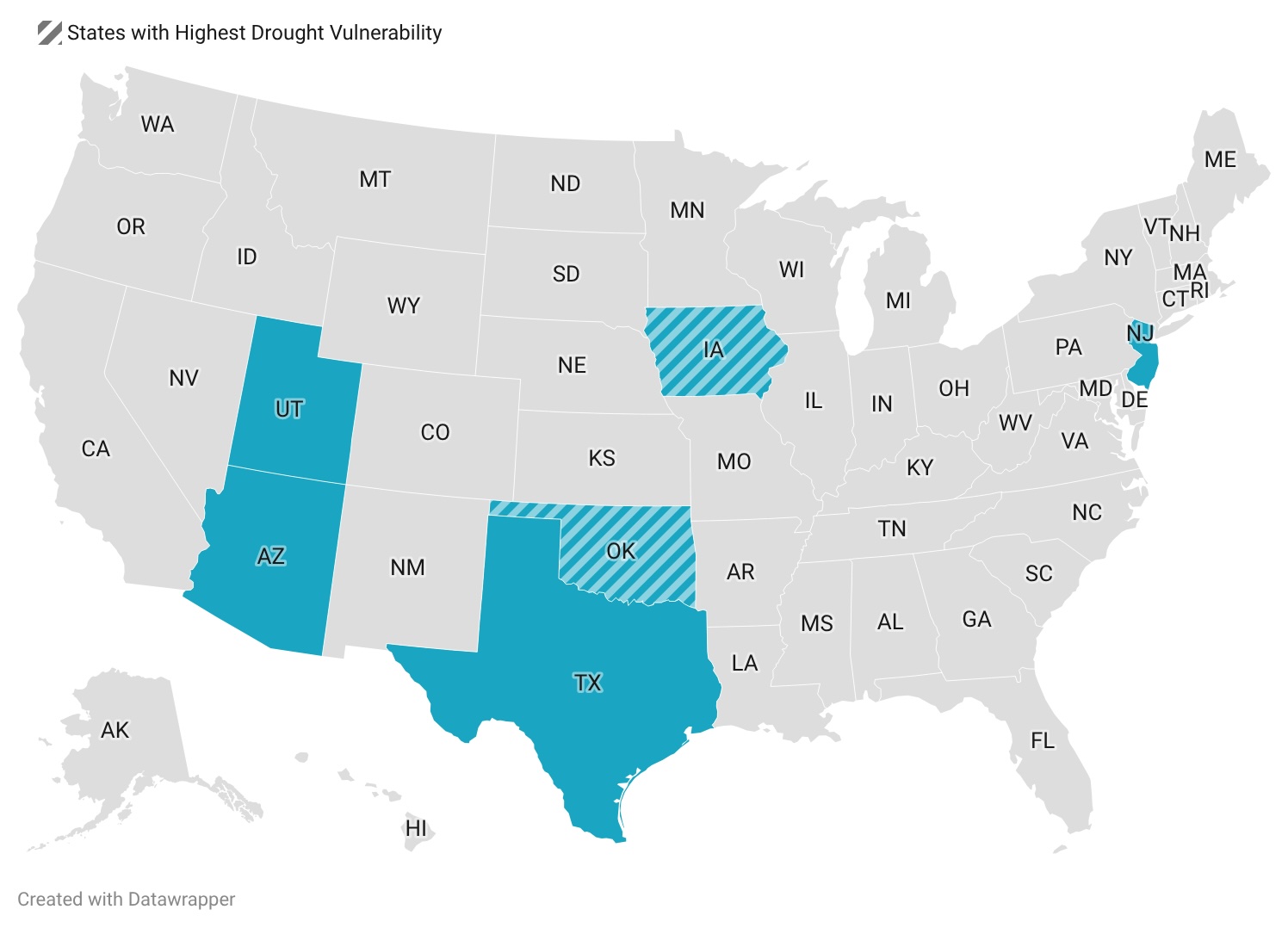

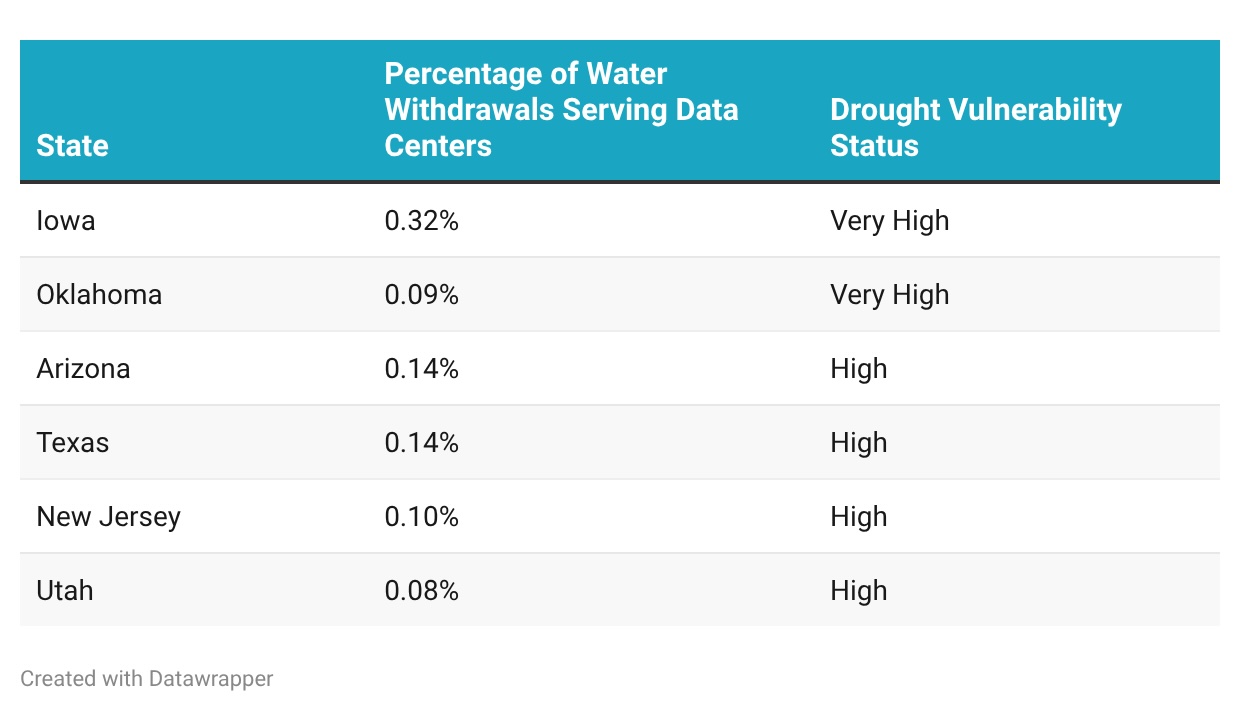

Rapid data center expansion threatens freshwater supply, as significant withdrawal of fresh water may lead to aquifer exhaustion, particularly in water-stressed areas. Like many impacts, water use and water pollution from data centers remain a black box; one study found that less than one-third of data centers actually report their water use. To identify states vulnerable to water stress, Climate XChange looked at 2023 data center demand, total water withdrawals in each state, and drought vulnerability by state. This analysis identified six states where data center water demand is most likely to contribute to water management problems, considering proportional water demand and state-level water resources.

Map 4. States with High Data Center Water Vulnerability

Of these six states, Arizona, Iowa, and Texas are also in the top 15 states for proposed data center buildout (“high growth data center states”). Data centers in Texas were expected to use at least 17 billion gallons of water in 2025, with one study finding their water demand equivalent to 793 gallons per megawatt-hour (MWh), and under a worst case scenario, as high as 45,701 gallons per MWh.

Table 5. States with Highest Percent of Data Center Water Withdrawals and Drought Risk

Water contamination from the use of evaporative cooling systems has been identified as an issue of concern, but this was not analyzed given the lack of data at the 50 state level. Comprehensive data on the types and quantities of effluent that may enter local watersheds from cooling operations are notably lacking across most states.

Policy considerations for addressing data center water use

Managing water use from data centers can take a two-pronged approach: first, require data centers to report how much water they are consuming and where that water is sourced from to better understand data center water usage, and second, require water conservation practices, water efficiency technologies, and the use of non-potable water to minimize on-site consumption of fresh water.

Taxes and Employment

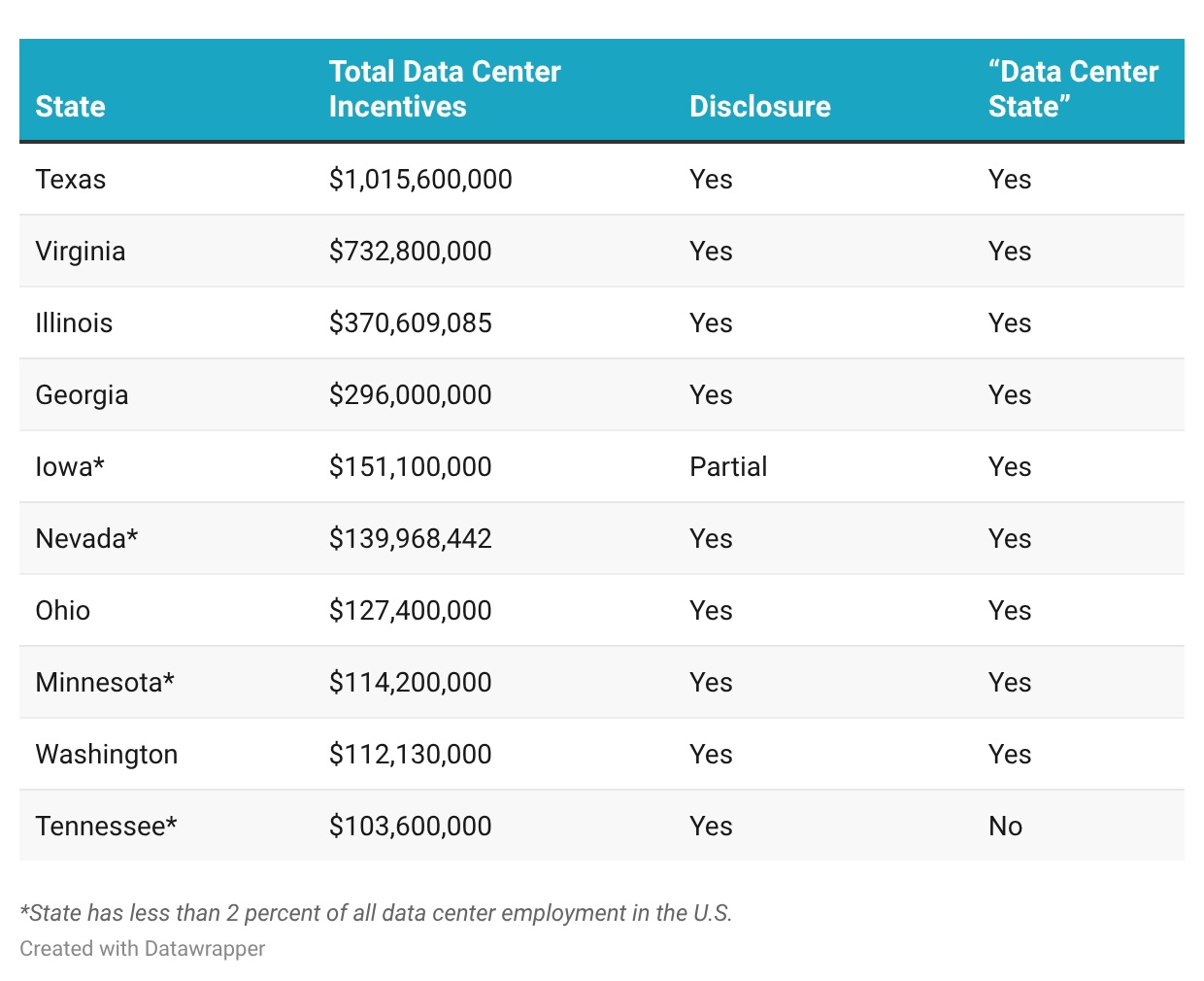

Under the promise of economic development and job creation, at least 37 states offer subsidies for data center development, typically in the form of property tax exemptions or sales tax exemptions for electricity or technology purchases. These incentives may be linked to aspects of a data center’s operations, like energy or water efficiency, or may be conditional on meeting an investment or job creation requirement, albeit for a small number of jobs. Regardless of how they are structured, states are investing massive amounts to steer data centers to their communities, and those funds may not be effectively achieving states’ aims.

To understand whether the incentives are benefitting states and their residents, we first have to understand how much states are spending to attract data centers. Unfortunately, there is a lack of transparency around incentives; about a dozen states that offer tax incentives are not required to disclose how much they are spending. For example, Pennsylvania isn’t required to disclose spending on data center-related tax incentives, but its tax credit just for equipment purchases costs the state $43 million in tax revenue annually, and the Governor’s office projects it will eclipse $50 million annually by the end of the decade.

The justification for these immense tax breaks is usually job creation, but data centers contribute little to local employment, especially permanent employment. Data center developments don’t create as many jobs compared to other capital-intensive industries like manufacturing. Indiana Michigan Power’s (I&M) own report shows that data centers create 100 times fewer jobs than other industries, by amount of power used. In Pennsylvania, Amazon touted its $20 billion investment by highlighting expected job creation, however, the 1,250 jobs it will create means the company is spending $16 million for every job created.

Three states estimate they lose between 52 and 70 cents for every dollar they spend on data center sales tax exemptions, which is only one type of incentive offered to the industry. With at least ten states offering more than $100 million in subsidies annually, this represents significant losses that could fund critical social services like education.

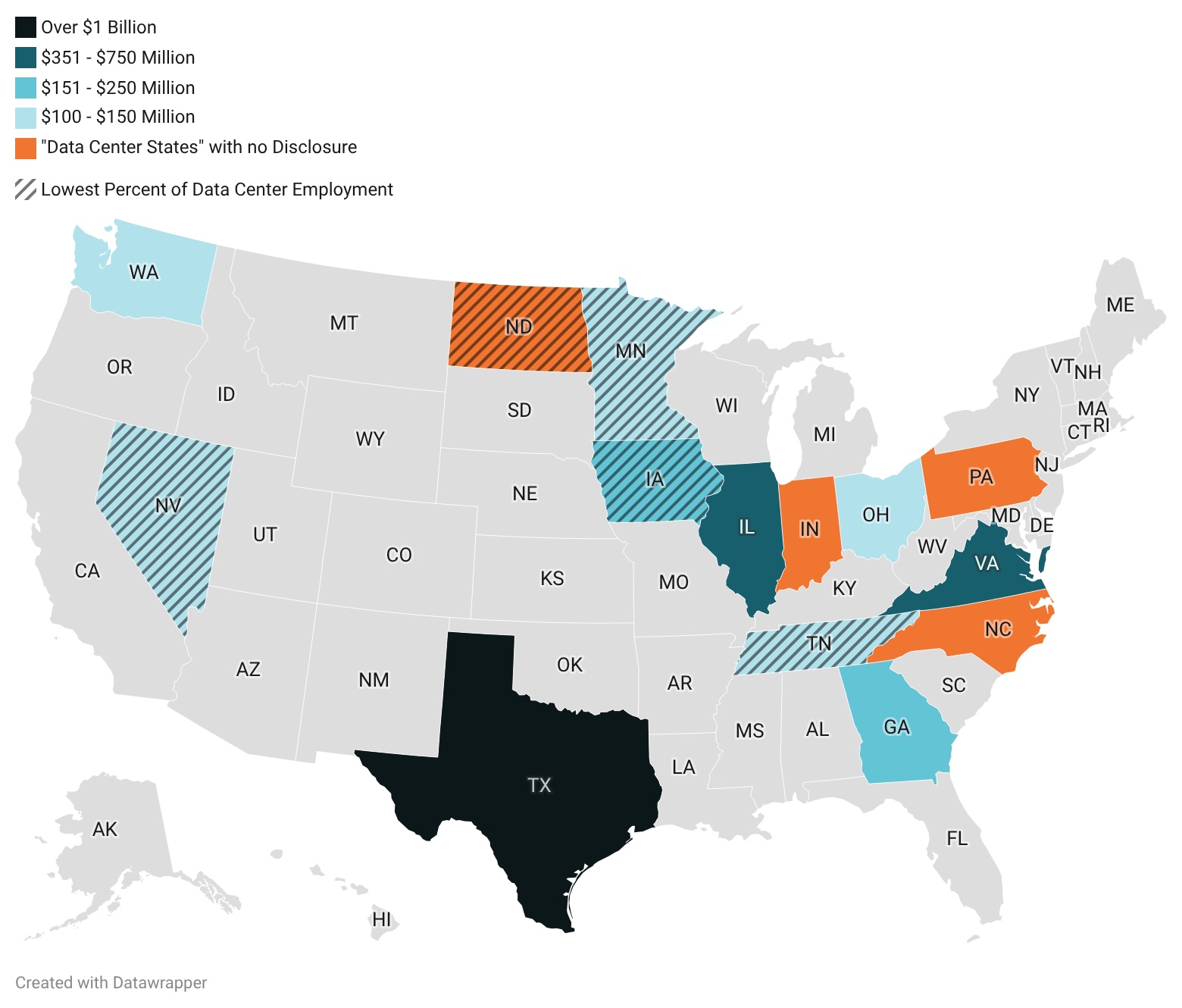

CXC compared those ten states to the concentration of data center employment in each state. Four of the ten states each employ less than two percent of the national data center workforce, suggesting a disconnect between data center incentives and employment outcomes. Tennessee stands out as the only state on this list that has high subsidies, low employment, but has not been identified as a “data center state.” Iowa also stands out for having high subsidies, low employment, but only requiring partial disclosure of subsidies, creating a murky picture on how much money is spent and where that money is going.

Map 5. Data Center Subsidies, Disclosure, and Employment Outcomes

Table 6. Highest Data Center Incentive States, Disclosure, and Employment

Policy considerations for addressing data center impacts on taxes and employment

Based on our analysis, states should not expand existing incentives or establish new ones. In states that already offer incentives, requiring disclosure of incentive amounts should be a first step for state policymakers. States can also reconsider these subsidies, or require that incentives are tied to stringent requirements around clean energy, energy efficiency, job creation, local investment, and energy affordability. Additionally, requiring community benefits agreements and long-term, well-paying employment opportunities that prioritize local hiring and union labor can help workers and local communities see some of the benefits they are promised.

Conclusions and What to Expect in 2026

Data center impacts are likely to be felt differently in every state, and this analysis offers only a preliminary assessment of which states may be most vulnerable to each different type of impact. Nevertheless, several themes emerge from this data, including:

- Leading states for data center development face multi-variable risks. Texas, for example, runs away from the pack in terms of potential greenhouse gas emissions from data centers, while also posing acute concerns about the cost of subsidies, the impact on water supplies, and electric reliability.

- Some smaller states may be particularly vulnerable to data center impacts. Iowa, for example, faces challenges from data center development on their greenhouse gas emissions, water resources, and energy affordability.

- Regional trends in data center development are beginning to take shape. For example, across the Great Lakes region, Pennsylvania, Ohio, and Illinois pose wide-ranging concerns from emissions and subsidies, to energy reliability and affordability.

These impacts will invite different types of policy response in every jurisdiction, and policymakers should consider the specific local dynamics that might open the door to regulating data centers in their own states. To help better equip policymakers with tools to confront data center development, Climate XChange will be releasing five policy toolkits in the coming months, examining the emerging state-level tools available to help address data center impacts on electric rates and reliability, water use, greenhouse gas emissions, transparency, and tax and employment outcomes.

In 2026, Climate XChange is committed to helping states identify trends, best practices, and model approaches to confront the wave of data center projects across the country, and help steer states towards the best climate, environmental, and social outcomes achievable.

Sign up for more information on our data center work and support for state actors.