Independent System Operators (ISOs) & Carbon Pricing: An Explainer

The player that nobody is talking about

A report by Lucy Davis-Hup, Emerson Johnston, Mridhu Khanna, and Sudhanshu Mathur, all of whom are State Carbon Pricing Network Fellows at Climate XChange.

Executive Summary

The next game-changing actor on the carbon pricing stage is one you may not have heard of — Independent System Operators (ISOs).

ISOs are non-governmental, non-profit organizations charged with overseeing the wholesale electricity market. They coordinate real-time electricity flow, ensure fair competition, and facilitate long-term grid investments. Today, seven regionally-based ISOs operate two-thirds of all electricity delivered in the United States, and are tasked with supplying affordable and reliable electricity. ISOs are not alone in shaping electricity markets and operating the electric grid. Federal bodies, state agencies, and other non-governmental groups play a significant role in determining the trajectory of electricity regulations, infrastructure, and operations.

Our current electricity generation model, one based largely on burning fossil fuels, fuels climate change — accounting for 27% of total U.S. emissions. Extreme weather conditions also endanger electric reliability, a core responsibility for ISOs. As a result, ISOs may be critical players in promoting cleaner energy generation and addressing climate change, especially through integrating carbon pricing into their operations. Recent carbon pricing developments at four ISOs — CAISO (California), NYISO (New York), PJM (13 states and D.C.), and ISO-NE (six New England states) — are promising, yet face challenges.

CAISO’s attempts to charge power coming in from out of state the carbon price paid by California utilities, but may not be doing so effectively. The body is a crucial player in the state’s Cap-and-Trade program, helping to guide policy decisions and outcomes through monthly emission reports. That said, it struggles to adequately report on and solve its resource shuffling issue, something that is proving to be the defining feature of the next decade of California’s emission reduction plans.

NYISO has proposed that they create a wholesale price on carbon equal to the social cost of carbon – which is at least ten times higher than the $5 per ton of CO2 charged under RGGI, which New York is part of. NYISO is paving the way forward for carbon pricing in wholesale energy markets. NYISO has drafted market rules in an effort to advance decarbonization set by RGGI and the State of New York. While emission reduction efforts have been largely led by state governments, NYISO is setting a precedent for wholesale electricity markets to impact decarbonization efforts in a major way. The outcome in New York will set the potential for state governments, ISOs, and federal agencies to align for climate action.

PJM is currently conducting a decisive study to determine the potential impacts of a carbon price on the region’s electricity markets, with a second phase that will map the regulatory reforms needed to implement a carbon price effectively. PJM has repeatedly stated that it will not be introducing a carbon pricing policy or proposal, but favourable study results may change that. Modelling potential impacts has been complicated, yet modestly promising — whether these results are strong enough to warrant further action is still to be seen.

ISO-NE’s President and CEO, Gordon van Welie, has voiced emphatic support for carbon pricing at a regional level. However, the ISO has not acted decisively so far, suggesting that it would need the support of the six states or the federal government before it introduces a carbon pricing proposal. Carbon pricing discussions are ongoing in the background, including an October 2019 symposium hosted by the MA Attorney General’s Office — ending with an agreement that “Meaningful regional carbon pricing will be necessary, but not sufficient, for decarbonization of the regional power system or economy.”

A changing grid and complex policy conditions will further challenge ISOs as they push for a cleaner electric future. ISOs are likely to become more prominent in the public domain, as different levers to achieve public climate goals are used. Undoubtedly, carbon pricing developments at ISOs signify the emergence of a new, critical policy opportunity to promote pro-climate changes to the nation’s sprawling, influential and high-emitting electric infrastructure.

What are ISOs?

Independent System Operators (ISOs) are non-governmental, non-profit organizations that oversee the wholesale electricity market for their corresponding regions. They coordinate real-time electricity flow, ensure fair competition, and facilitate long-term investments. ISOs follow the guidelines and regulations issued by the Federal Energy Regulatory Commission (FERC), while working in conjunction with stakeholders across the electricity grid. Today, seven regionally-based ISOs operate two-thirds of all electricity delivered in the United States, and are charged with supplying affordable and reliable electricity.

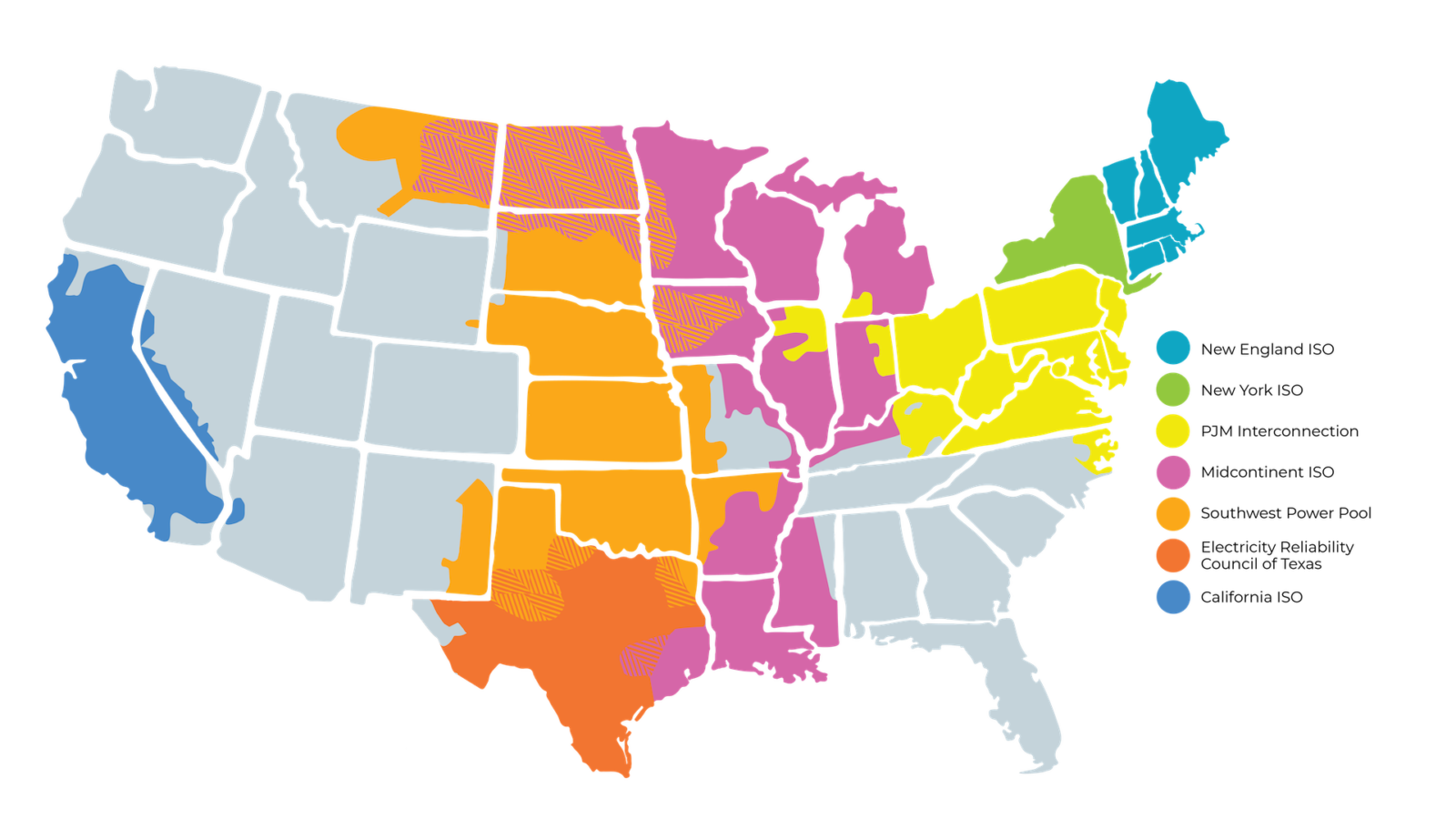

Map of U.S. ISOs and RTOs.

History

Understanding ISOs depends on a fundamental comprehension of the electricity grid. Today’s grid is centralized, with electric power being generated at large-scale facilities before being dispatched great distances across the country. The grid encompasses three primary components: generation, transmission, and distribution. Most of the country’s electricity is generated by close to 10,000 power plants, which often rely on the burning of nonrenewable fossil fuels. Then, electricity is sent across 700,000 miles of transmission lines to substations all over the country. Through millions of miles of wires, electricity is finally distributed to its end users, powering residential, commercial, and industrial infrastructure.

For a deeper look at the electric grid, check out this 2020 CXC article: Why Grid Modernization Promises a Stronger Electrical, Environmental and Economic Future

Given the sprawling electricity infrastructure that interweaves through many different jurisdictions, regulating the wholesale and retail electricity markets is complex. Before the advent of ISOs, there was no distinction between wholesale and retail electricity markets. As it seemed, market dynamics — high infrastructure costs and economies of scale — supported the formation of a single entity (the ‘natural monopoly’) to generate, transmit, and distribute electricity.

| High Infrastructure Costs | Economies of Scale |

| Building and operating power plants, transmission lines, and distribution stations requires enormous investment, which makes it difficult for new companies to enter the electricity market. | The average cost of producing electricity decreases as more electricity is sold, allowing larger producers to naturally outcompete smaller ones. |

Monopolies are often frowned upon, since they typically bring about higher prices and lower product quantity and quality, along with engaging in unfair competitive practices. But with high infrastructure costs and economies of scale, combined with the need to provide a public service, a natural electricity monopoly seemed to be the most efficient path forward. To protect consumers from high prices and poor product quality, natural electricity monopolies (known as vertically integrated utilities) would be heavily regulated.

Even today, about one-third of the U.S. electric power supply continues to be managed by vertically integrated utilities, where they are wholly responsible for generating, transmitting, and distributing electricity. If these utilities are not involved in interstate transmission or wholesale electricity markets, they do not fall under FERC jurisdiction – but are thoroughly regulated by state public utility commissions.

In the 1970s, policymakers began to reevaluate the natural monopolistic model of electricity provision. Rising fuel prices, growing environmental concerns, emerging technological innovation, and a push for greater economic efficiency contributed to this rethinking. Large-scale monopolistic utilities were underperforming with regards to their mandates, as the potential for competition was restrained. Partly as a result of the underperformance, utilities began to organize into ‘power pools,’ where they would share infrastructure with each other to reach more customers. By coordinating, utilities were able to reduce operating and maintenance costs, while improving electricity’s reliability through expanded reserve capacity and initiating long-term planning.

Promising results from restructuring the natural gas and telecommunications sectors further encouraged policymakers to develop ISOs, as a method of enabling competition while maintaining system operations and reliability. FERC realized that only the transmission lines, not generators or distribution substations, constituted the conditions for a natural monopoly. This realization was driven by promising small-scale and cost-effective innovation on the generation and distribution front, in opposition to the theories of high infrastructure costs and economies of scale. FERC opted to split the electricity market into wholesale and retail components, while pushing for the dissolution of vertically integrated utilities. FERC posited that an entity free from undue influence could be charged with fairly operating the wholesale electricity market. This entity, known as an independent system operator (ISO) or regional transmission organization (RTO), would manage power flow across transmission lines based on the transactions taking place in the wholesale electricity market. Load-serving entities (LSEs) would purchase electricity from power generators in the wholesale market, before reselling that electricity to the final consumer (residential, commercial or industrial) in the retail market.

Key FERC Orders

Through the Energy Policy Act of 2005 and similar legislation at the state level, regulations constraining the structure and operations of utilities were repealed, while renewable energy, tax incentives, and energy efficiency were promoted. But, the key guidance on establishing ISOs from FERC came earlier, through Orders 888, 889, and 2000. FERC believed that ISOs could fulfill three needs of the evolving electricity system: market competitiveness, real-time system coordination, and long-term infrastructure planning. Critically, ISOs had to be independent from the different electricity stakeholders to ensure fairness in the market of electricity. ISOs would thus enable more power generators (often small-scale and renewably-sourced) to compete on a more equal footing, while also maintaining the short-term and long-term reliability of the system. FERC Orders 888, 889, and 2000 clearly delineated the changes that led to the formation of ISOs.

FERC ORDERS

Order 888

Passed in 1996, Order 888 mandated non-discriminatory access to transmission systems, a game-changer for the electricity industry. Previously, utilities favoured their own generators to be used in delivering electricity along their own transmission lines to end-use consumers. Though other generating companies could strike deals with transmission owners, utilities held the upper hand in the negotiations, since they were the sole purchasers of generated electricity.

To prevent discrimination, FERC ruled that any power generator could supply electricity through transmission lines that must be open to all, regardless of who owned the transmission lines. In order to ensure that the generators were treated fairly, FERC further ruled that the utility must provide equal transmission service to all power generators. FERC ordered transmission operators to file Open Access Transmission Tariffs (OATT), to specify the procedures being used to ensure non-discriminatory transmission access. Recognizing the need for independence towards preventing discrimination, FERC encouraged the voluntary development of ISOs to facilitate the unbiased operation of transmission lines.

Order 889

Also passed in 1996, Order 889 required each transmission owner to create and maintain a publicly accessible Open-Access Same-time Information System (OASIS). OASIS would uniformly provide the necessary market information — prices, reserve capacity, current demand, and so on — preventing discrimination by giving all concerned stakeholders the same level of market information.

Order 2000

In 1999, Order 2000 further encouraged transmission-owning entities to form an ISO (or RTO, as referenced in the order) by defining its minimum characteristics and functions. In order to ensure a fair electricity market, the ISO must be independent from all market participants. As such, ISOs would fairly represent all stakeholders, would not be owned by any market participant, and would not provide any stakeholder class with advantageous control over decision-making. It should act as the sole authority on providing transmission services, administrating OASIS, and supplying ancillary services. FERC also charged ISOs with monitoring the wholesale electricity market, meeting reliability standards, planning future transmission infrastructure, and coordinating with other regions. Additionally, ISOs would not engage in retail electricity markets, own electricity infrastructure (or stakes in affiliated companies), or enact energy policy.

Key ISO Functions

ISOs were placed in an unconventional situation: they would be operating electricity assets that they did not own. In order to achieve their primary functions, ISOs facilitated the creation of four classes of wholesale energy markets (the day-ahead, real-time, capacity, and ancillary services markets) to maintain system reliability. The ISO acts as the operator of these markets, providing market information through its OASIS and a virtual marketplace, while ensuring that transactions occur smoothly. There are three types of electricity sales take place across these markets: between large, vertically integrated utilities (to minimize each other’s costs or improve reliability); from vertically integrated utilities to load-serving entities (LSEs, those who sell power in the retail electricity market to end-use consumers); and from independent (non-utility) power producers (IPPs) to utilities or LSEs.

TYPES OF ELECTRICITY MARKETS RUN BY ISOs

- Day-Ahead Market: One day before electricity is due to be supplied, generators will offer their electricity to utilities at particular prices in this market, based on the ISO’s projection of electricity demand for the following day.

- Real-Time Market: Though electricity supply has been secured one day in advance, there are usually fluctuations in actual electricity demand on the day itself. In order to adjust electricity supply as per actual demand, the ISO can facilitate electricity purchases or sales for utilities in real-time. It does this by accepting bids and offers put up by generators, allowing electricity supply to be responsive to changes in demand.

- Capacity Market: In order to ensure future investment in generation assets, the ISO operates a marketplace that allows for purchases and sales of future generation capacity. Generators promise a particular supply capacity of electricity to utilities several years in advance of when they are actually required.

- Ancillary Services Market: To ensure reliability, the ISO maintains access to sizable backup generation capacity, in the case of an unexpectedly high demand or a generator outage. This market allows for the sales of a range of backup resources.

- Reserves: capacity that can be synchronized with the grid quickly, usually between 10-30 minutes.

- Regulation: capacity that can quickly adjust its output to ensure stability in system frequency.

- Blackstart capability: key power plants that can restart the transmission system in case of a blackout.

- Reactive power: power that is used to maintain voltage and move current.

Essentially, ISOs serve three primary functions: ensuring market competitiveness, dispatching power flow, and facilitating long-term transmission planning. Each market plays a role in ensuring fairness by uniformly providing market information that helps determine prices, supply, and demand. When transactions are completed on the day-ahead, real-time, and ancillary services markets, the ISO knows which generators are to be used, and dispatches their electricity production accordingly across transmission lines. Through the capacity market and its analysis of electricity data, the ISO encourages investment in future generation and transmission assets to ensure the long-term reliability of the grid. Each ISO operates such markets, with their market regulations subject to FERC review.

WHAT IS CLEARING THE MARKET?

“Clearing the Market”

ISOs go through a process known as “clearing the market” when determining which generators are used at a certain time. Generators bid their generation capacity and the lowest prices at which they would be willing to sell their electricity for, but these prices differ due to their different production methods. When setting the market price for wholesale electricity, the ISO begins by adding up the capacity provided by power producers, from least to most affordable, until supply meets demand. At this point, the ISO confirms that price as the wholesale market price for electricity. All producers and sellers exchange electricity at this price point, regardless of the generators’ initial bids. This selection process forces more expensive generators to become more competitive, or simply be forced to exit.

Of particular note, renewable energy sources are extraordinarily cheap (on a marginal production cost basis) electricity producers. Bids from renewable energy producers are lower than those using fossil fuels, resulting in ISOs often opting for renewable sources before selecting other generation types. Increasing the capacity of renewable energy producers will dramatically lower the marginal cost of electricity (across entire wholesale and retail markets), as supply meets demand at an earlier, lower price. Carbon pricing can play a key role in reducing the competitiveness of fossil fuel producers, as a path to stimulating cheaper and cleaner electricity generation.

How do ISOs interact with federal bodies, state agencies, and other organizations?

In addition to covering the major national stakeholder groups, this section describes organizations that are specific to Massachusetts and the New England region, to offer specific examples of what organizations are involved. New England- or Massachusetts-specific organizations mentioned here likely have counterparts in the different states and regions of the country.

ISOs do not operate in a vacuum. They are surrounded by a host of different organizations, with differing mandates and powers. In combination with the ISO, these organizations play an important role in determining the regulation of electricity markets today. Below are the key players associated with the electricity industry.

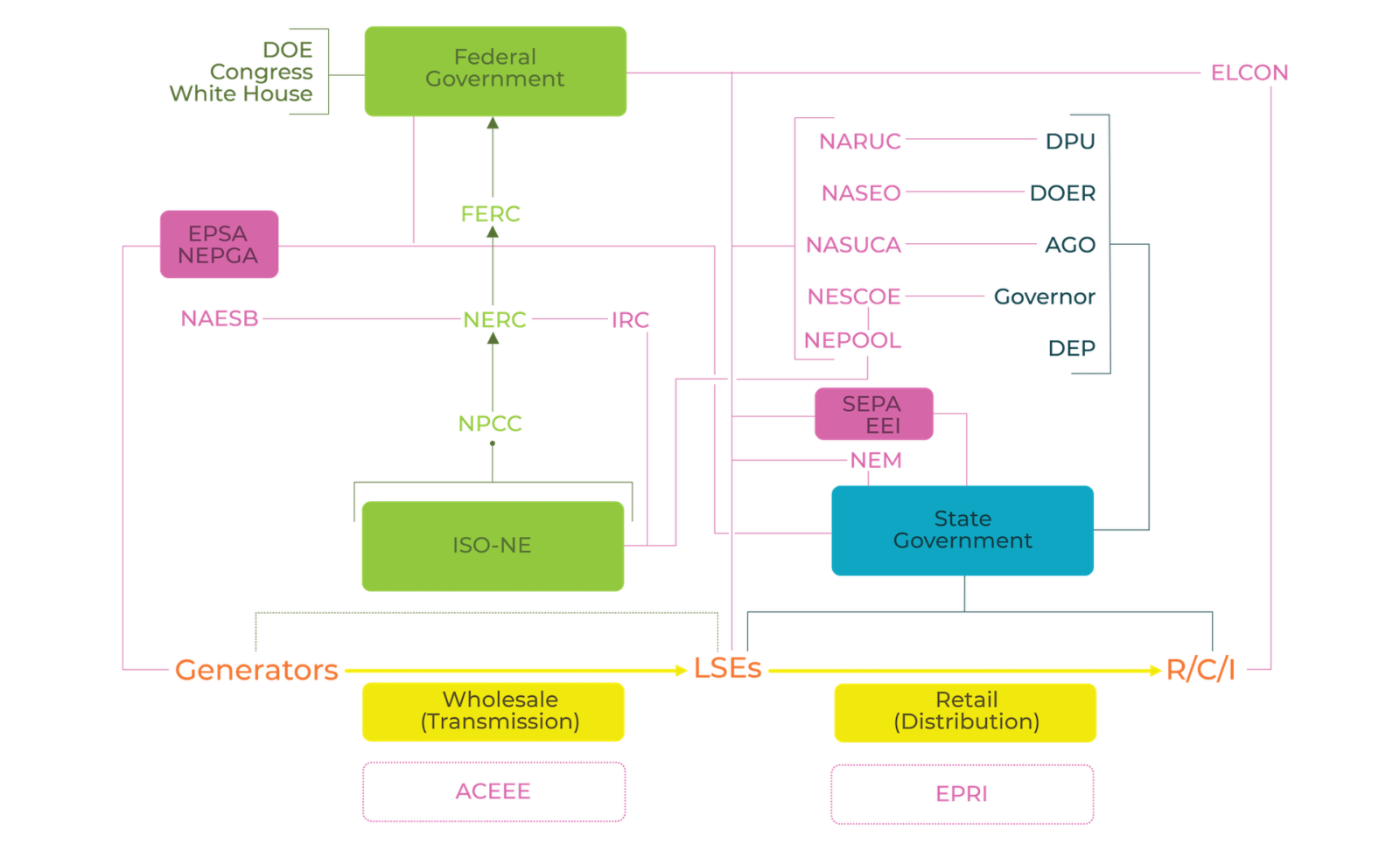

The above graphic describes the structure of electricity regulation in Massachusetts, highlighting both the formal and informal structures of influence. The lines connect organizations that work with each other (pink, predominantly), and all vertical hierarchies point to levels of authority. Similar organizations and structures exist in competitive electricity markets in the United States, but those organizations are not included here. This diagram's structure does not apply to traditionally regulated markets (across ~30% of the country), where no wholesale electricity market structure (no ISO) exists. Please use the accompanying descriptions to understand all facets of the diagram. Key: Green = federal/regional bodies and formal regulatory structure; Black = state bodies and their formal regulatory structure; Orange = principal electricity agents; Pink = non-profits and trade associations.

LSEs: Load-Serving Entities (the companies that the ordinary consumer purchases electricity from)

R/C/I: Residential, Commercial and Industrial consumers, the final purchasers and users of electricity

FERC: Federal Energy Regulatory Commission (regulates interstate transmission of electricity)

NERC: North American Electric Reliability Corporation (sets reliability standards, reports to FERC)

NPCC: Northeast Power Coordinating Council (regional entity under NERC for Northeast US)

DOE: US Department of Energy

DPU: MA Department of Public Utilities (regulates retail electricity market in MA – only investor-owned utilities)

DOER: MA Department of Energy Resources (serves on NASEO)

DEP: MA Department of Environmental Protection

AGO: MA Attorney General’s Office (serves on NASUCA)

EPSA: Electric Power Supply Association (represents and advocates for electricity generators)

NEPGA: New England Power Generators Association (represents and advocates for electricity generators)

NASEO: National Association of State Energy Officials (represents nationwide Governor-appointed energy officials; MA – DOER Commissioner)

NARUC: National Association of Regulatory Utility Commissioners (represents nationwide public utility commissions; MA – DPU Commissioner)

NASUCA: National Association of State Utility Consumer Advocates (represents nationwide state consumer advocates, appointed by law; MA – AGO Energy Chief)

NESCOE: New England States Committee on Electricity (represents governors of New England states)

NAESB: North American Energy Standards Board (forum to develop reliability standards, with NERC and IRC)

ACEEE: American Council for an Energy-Efficient Economy (nonprofit that works with everybody to advance energy efficiency)

EPRI: Electric Power Research Institute (nonprofit that conducts key research for electricity stakeholders)

ELCON: Electricity Consumers Resource Council (represents industrial consumers of electricity)

SEPA: Smart Electric Power Alliance (nonprofit that works with everybody for a smarter electric grid)

EEI: Edison Electric Institute (represents and advocates for investor-owned utilities)

NEM: National Energy Marketers Association (represents wholesale and retail electricity marketers)

IRC: ISO/RTO Council (works on reliability standards with NERC and NAESB, but also convenes ISOs)

NEPOOL: New England Power Pool (brings together electricity stakeholders to work with ISO-NE)

Electricity Agents

The primary agents of the electricity market are the generators, the load-serving entities (LSEs), and the residential, commercial, and industrial (R/C/I) consumers. Generators are the power plants using energy sources to create electricity. Their electricity is sold to LSEs on the wholesale electricity market, which is operated by ISOs. LSEs (what we usually understand as utilities) then resell electricity on the retail market to the final consumers of electricity: R/C/I customers. Each of these three primary agents are regulated in their practices by various other federal and state bodies, but are also often represented through unique associations to voice their opinions on regulatory practices.

Federal Bodies

Congress, the White House (WH), and the Department of Energy (DOE)

These three federal bodies work together to set the high-level priorities and policies for the electricity markets (as well as many other policy areas), before passing on the more involved regulatory aspects to specially-designated federal and state agencies. With Congress and the WH being elected by the public, along with the Secretary of Energy being nominated by the President and confirmed by the Senate, these three bodies are much more political in nature, and are more heavily influenced by electoral forces. As a result, they are all frequently approached by different electricity stakeholders for major changes to national electricity policies.

The Federal Energy Regulatory Commission (FERC)

FERC, under the U.S. Department of Energy (DOE), is the federal agency tasked with regulating the interstate transmission and wholesale selling of electricity. FERC’s responsibilities include overseeing reliability standards for the electric system, promoting the development of energy infrastructure, and ensuring fairness in interstate electricity markets. Through orders in the 1990s, FERC laid the groundwork for the establishment of ISOs in its pursuit of making electricity markets more competitive. It has since served as the ISOs’ supervisor, regulating their interstate operations and energy infrastructure planning. They approve the rates, terms, and conditions governing the sale of transmission services and wholesale electricity. It is important to remember that FERC does not have jurisdiction over retail electricity markets (similar to ISOs) or intrastate electricity commerce (the responsibility of state public service commissions). Given its significant responsibility of maintaining market fairness, FERC is an independent regulatory agency — though political influence is always possible — with only federal courts being able to review its decisions. In addition, FERC is also involved in the regulation of interstate transmission of oil and gas.

The North American Electric Reliability Corporation (NERC)

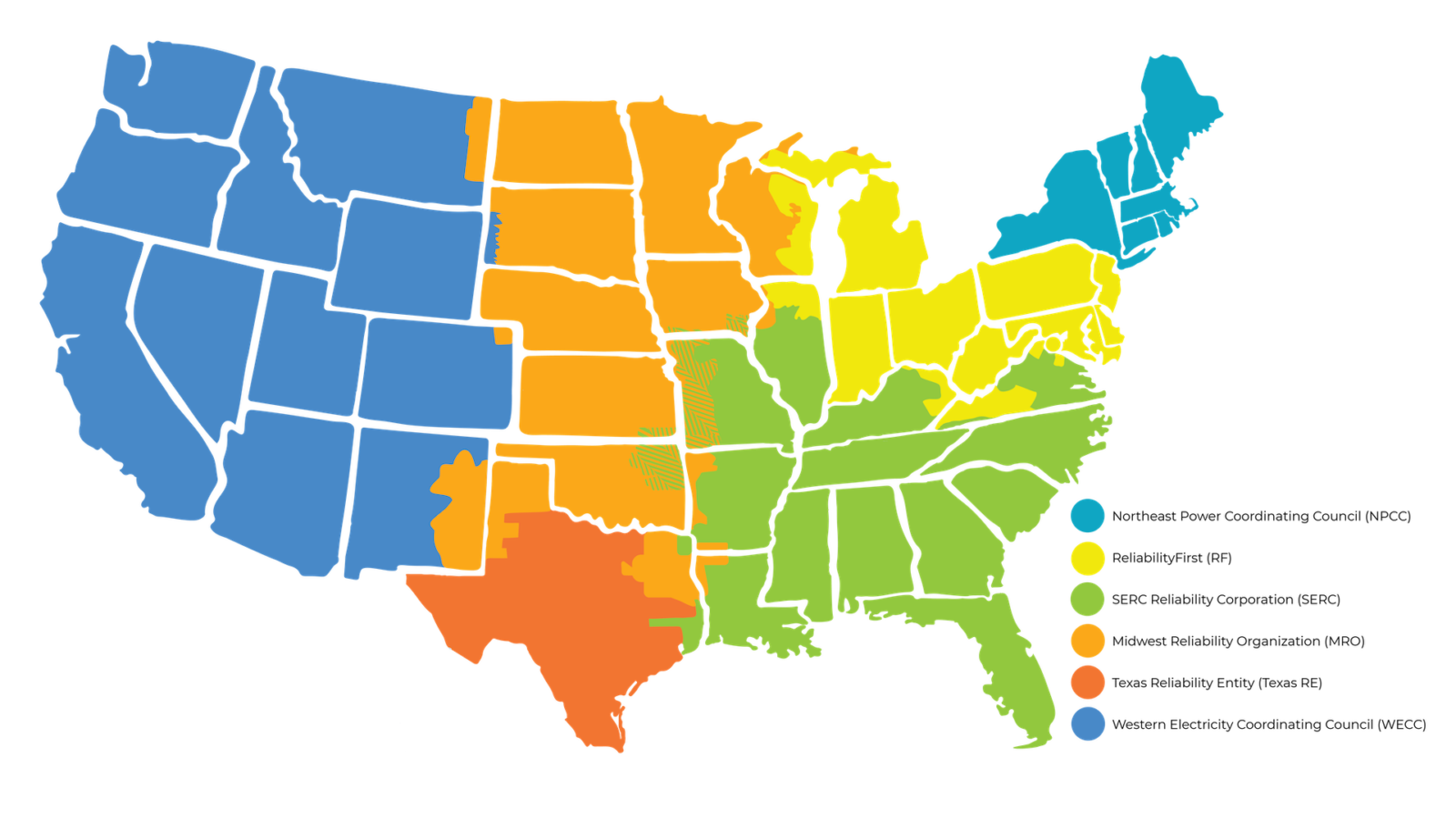

NERC, a not-for-profit regulatory body, is tasked with monitoring and assessing the reliability of the electric grid. When designated by FERC as the Electric Reliability Organization (ERO) in 2006, NERC began developing and enforcing reliability standards. Overseeing the electric reliability for more than 400 million people, NERC’s jurisdiction includes the continental U.S., Canada, and the northern portion of Baja California, Mexico. NERC has opted to delegate its responsibilities to seven regional reliability councils, which are similarly tasked with monitoring and enforcing compliance with electric reliability standards. These regional reliability councils are:

- Northeast Power Coordinating Council (NPCC)

- ReliabilityFirst (RF)

- SERC Reliability Corporation (SERC)

- Midwest Reliability Organization (MRO)

- Texas Reliability Entity (Texas RE)

- Western Electricity Coordinating Council (WECC)

Map of NERC regional reliability councils.

State Agencies

State regulatory agencies charged with regulating electric utilities (directly and indirectly) also influence the operations of the ISO, as does the rulemaking of the Governor and legislative chambers. Below are the agencies relevant to the regulation of electricity in Massachusetts, which all report to the Executive Office of Energy and Environmental Affairs.

Department of Public Utilities (DPU)

The DPU is the state body most directly involved in regulating utilities (including those providing electricity) in Massachusetts, aiming for safety, efficiency, and affordability. As the public service commission of the state, the DPU’s regulations are key to enabling a fair retail electricity market.

Department of Environmental Protection (DEP)

DEP enforces laws that protect the environment of Massachusetts, including air, land, and water. This jurisdiction expands to enforcing environmental regulations on utilities, further influencing their rates and services.

Department of Energy Resources (DOER)

DOER governs Massachusetts’s energy resources, with a particular emphasis on encouraging clean energy, energy efficiency, and resilient energy strategies. The agency plays a key role in overseeing energy producers in the state, and ensures that they are able to participate in electricity markets.

Office of Ratepayer Advocacy, at the Attorney General’s Office (AGO)

The AGO of Massachusetts serves as the state’s ratepayer advocate, representing the voice of consumers on utility prices and services. Notably, AG Maura Healey has promised incorporating “the cost of climate response” into electricity prices, in order to mitigate climate change impacts. Currently, Rebecca Tepper serves as the Energy Chief at the AGO, as well as Massachusetts’ representative to NASUCA.

Other Groups

A diverse set of nonprofits and industry associations play a role in the policymaking process surrounding the electric industry. These organizations can act as simple forums for discussion, or as advocacy groups pursuing particular regulatory goals. Some are tangentially related to the electricity industry, while some are completely centralized on the particular work of ISOs. (The list below is not comprehensive.)

The ISO/RTO Council (IRC)

The IRC is an industry association that brings together ten ISOs/RTOs operating in the U.S. and Canada, allowing them to work collaboratively on a range of operations: communications, planning, regulatory and legislative initiatives, standards review, technology and markets.

The North American Energy Standards Board (NAESB)

The NAESB acts as a forum to develop reliability standards (often in partnership with NERC and IRC) for the wholesale and retail electric and gas industries, convening the various stakeholders: ISOs, end users, distributors, transmission, generation, marketers, and technologists.

The National Association of Regulatory Utility Commissioners (NARUC)

NARUC is a nonprofit that represents all the state public service commissions (which regulate utilities, like electricity, in their respective states) at the federal level, amplifying and unifying their collective voice to influence federal utility policies. The Department of Public Utilities (DPU) participates in NARUC, representing Massachusetts.

The National Association of State Utility Consumer Advocates (NASUCA)

NASUCA is an association that brings together state-appointed ratepayer advocates, to elevate the representation and participation of consumers in regulating utilities at the state and federal levels. The Attorney General’s Office (AGO) participates in NASUCA, representing Massachusetts

The National Association of State Energy Officials (NASEO)

NASEO is a non-profit association made up of the governor-designated state energy officials from across the nation, which serves as a platform for learning, cooperation and advocacy at the federal level. The Department of Energy Resources (DOER) participates in NASEO, representing Massachusetts.

The New England States Committee on Electricity (NESCOE)

NESCOE represents the governors of six New England states, in offering their interests and policy perspectives on promoting a robust electric system under the guidance of ISO-NE.

The New England Power Pool (NEPOOL)

NEPOOL is a voluntary association made up of hundreds of electric market stakeholders that contribute their insights on ISO-NE’s operations. In coordination with NESCOE, NEPOOL forms the Regional State Committee (RSC) for the New England region — a body devised by FERC to harmonize state views on regional electric market activities.

The New England Power Generators Association (NEPGA)

NEPGA is a trade association for electricity generator companies in New England, which advocates for sound and competitive electric market policies.

The Smart Electric Power Alliance (SEPA)

SEPA is a nonprofit dedicated to a clean energy future by aiding the transition to cleaner and smarter electricity, and by working extensively with utilities.

The New England Power Pool (NEPOOL)

NEPOOL is a voluntary association made up of hundreds of electric market stakeholders that contribute their insights on ISO-NE’s operations. In coordination with NESCOE, NEPOOL forms the Regional State Committee (RSC) for the New England region — a body devised by FERC to harmonize state views on regional electric market activities.

The New England Power Generators Association (NEPGA)

NEPGA is a trade association for electricity generator companies in New England, which advocates for sound and competitive electric market policies.

The Smart Electric Power Alliance (SEPA)

SEPA is a nonprofit dedicated to a clean energy future by aiding the transition to cleaner and smarter electricity, and by working extensively with utilities.

Electric Power Supply Association (EPSA)

EPSA represents energy suppliers, and largely focuses on advocating for competitive and fair wholesale electricity markets.

Electric Power Research Institute (EPRI)

EPRI is an independent nonprofit organization that specifically conducts a range of electricity industry research projects for electricity market stakeholders.

American Council for an Energy-Efficient Economy (ACEEE)

ACEEE is a nonprofit organization that works at all levels and with all stakeholders to harness the full potential of energy efficiency.

Electricity Resource Consumers Council (ELCON)

ELCON represents large industrial consumers of electricity, as they advocate on federal and state policies affecting the price, availability, and reliability of electricity service.

Edison Electric Institute (EEI)

EEI is an association that represents all investor-owned utilities in the U.S. (who are responsible for delivering to 72% of all electricity customers), and provides public policy leadership.

National Energy Marketers Association (NEM)

NEM is a non-profit trade association that represents both wholesale and retail marketers of electricity (and related industries), and advocates for policies at the federal and state levels.

Why are ISOs relevant to carbon pricing?

ISOs could become key strategic players in mitigating and adapting to climate change, and they are increasingly considering carbon pollution pricing as a powerful tool towards those efforts.

Climate change is principally caused by greenhouse gas emissions from human activity — in the United States, 27% of emissions are attributable to electricity generation. Two-thirds of the nation’s electricity flows under the supervision of ISOs — the organizations that are in chief positions to determine which sources of electricity (fossil fuels or renewable energy) will be used. Not only are ISOs responsible for a substantial portion of the nation’s emissions, they are legally entrusted with the short-term and long-term reliability of the electricity system. Extreme weather events, public health impacts, and the other devastating consequences of climate change will profoundly impact ISOs’ ability to provide electricity.

As part of its “clearing the market” process, ISOs usually opt for all available renewable energy sources, since they are the cheapest available generators on a marginal production cost basis. However, renewable energy sources make up only 18% of national utility-scale generation capacity. Achieving net-zero emissions by 2050 — a timeline many experts, reports, and organizations consider absolutely critical to mitigate climate change — will depend on a rapid increase in renewable energy capacity, along with a correspondingly rapid decrease in the hazardous use of fossil fuels.

Implementing carbon pricing through ISOs represents an opportunity to further drive this crucial shift, especially when substantial numbers of state, local and national lawmakers have failed to adequately promote such a change. ISO-led carbon pricing could not only move legislatures forward, but promote a sound market-based climate change mitigation policy with direct regional economic influence. The discussion surrounding this possibility has spiked, with electricity stakeholders calling on FERC — as recently as April 2020 — to hold a technical conference on integrating carbon pricing into wholesale electricity markets.

Status of carbon pricing at ISOs

California Independent System Operator (CAISO)

Established in 1996 pursuant to Assembly Bill 1890 passed as a part of California’s electricity restructuring effort, the CAISO has made very important strides with regard to nationwide greenhouse gas (GHG) emissions targets. Through the Monthly GHG Emission Tracking Report and the Daily Outlook for Emissions, the operator remains at the forefront of emission transparency. (The Monthly GHG Emission Tracking Reports track statewide emissions monthly, while the Daily Outlook does the same on a daily basis, though neither report uses official data in their estimations. The official GHG emission data can be found with the California Air Resource Board)

The CAISO also conducted several studies to determine the viability of an expanded regional grid and a bulk of their primary research focuses on the viability and implementation of one in the near future – a result of the California Senate Bill 350, passed in 2015, that directed the operator to study the impacts of a regional western U.S. grid. The study found that a Western states energy market will yield significant environmental and economic benefits to California and the West, including cost savings to ratepayers, reduced air pollution, new jobs, market efficiencies, and improved transmission planning.

Basics of carbon pricing in California (history, benefits, program development)

Launched in 2013, the California Cap-and-Trade System is a flagship program in the state’s carbon reduction efforts and was designed to contribute 20% of total reductions through 2020, per CA’s 2008 Scoping Plan. It was designed as a “backstop” in case other measures failed or underperformed. As the first multi-sector cap-and-trade program in North America and the fourth largest in the world, California’s cap-and-trade system has provided invaluable information regarding the creation and management of regional cap-and-trade systems as whole.

The system, which now covers about 85 percent of the state’s emissions and invests billions of dollars in emissions reduction projects, initially began in 2013 as a rule only applied to stationary emissions sources, such as electric power plants and industrial facilities,, that emit 25,000 tons of carbon dioxide equivalent per year or more. The program was later extended to mobile emissions sources, via the regulation of fuel distributors meeting the 25,000-metric ton threshold, in 2015. Since then, the Californian system has become a central component of the state’s comprehensive approach to reduce greenhouse gas emissions to 1990 levels by the year 2020, 40 percent below 1990 levels by 2030, and 80 percent below 1990 levels by 2050. The state also intends to reach economy-wide carbon neutrality by 2045.

Since the program began, statewide greenhouse gas emissions have reduced significantly, with multiple reports citing figures around a 5.3 percent decline through 2017. The state went on to surpass their 2020 emissions goals four years earlier than planned in late 2016. Though, due to the economic recession, complementary policies, and shifting contracts for imported electricity, emissions have decreased faster than expected. The cap-and-trade program has played a smaller role than expected in achieving the state’s 2020 emissions target by 2016 with its actual contributions still being up for question. According to Propublica, “the Chris Busch of Energy Innovation, a climate policy think tank, […] estimates that in 2015 and 2016, cap and trade was responsible for only 4% to 15% of the state’s reductions.” Moreover, a recent report out of UC Berkeley suggests that recent reduction in California’s GHG emissions cannot be attributed to cap-and-trade but to other factors such as renewable portfolio standards and energy efficiency policies. That said, the Center for Climate and Energy Solutions maintains that at least some of this reduction can likely be attributed to California’s cap-and-trade program.

How does carbon pricing work in conjunction with CAISO in CA?

The relationship between the California Independent System Operator (CAISO) and the state’s cap-and-trade system continues to evolve with every policy made regarding carbon emissions in the state. That said, the two entities primarily interact with regard to energy imports and through the problem the state continues to have with resource shuffling.

What is most unique about the CAISO is the emission credit it receives for exported electricity, something that can be credited as creating the operators resource shuffling problem. Resource Shuffling — replacing cleaner sources of electric power with dirtier and cheaper sources of energy — is arguably the largest problem facing the ISO as of 2020. Because the import and generation of energy in California are subject to the state’s Cap-and-Trade Program, generators and importers that operate under the current ISO footprint have begun redistributing their sources of energy to accommodate CAISO requirements. While California has seen an overall increase in the use of clean energy, states that use the same generators are seeing opposite results.

Though the CAISO claims to avoid potential double-counting of emissions for California BAs, the effects of such a policy have yet to be seen.

New York Independent System Operator (NYISO)

NYISO’s carbon pricing proposal was introduced in an effort to harmonize state efforts to meet New York’s carbon emissions reduction goal and the operation of the wholesale energy market. In conjunction with the New York State Department of Public Service, the New York State Research and Development Authority, and other stakeholders, NYISO formed the Integrating Public Policy Task Force (IPPTF) to explore the possibility of incorporating a social cost of carbon into the wholesale cost of electricity. Ultimately, the task force produced the IPPTF Carbon Pricing Proposal to provide the basics of the market design in the next steps for implementation.

For the carbon pricing proposal to go into effect, it must move through and be approved by a series of groups beginning with the NYISO stakeholders committee. Composed of stakeholders from across sectors, the committee includes environmental advocacy groups, energy suppliers, community organizations, regulatory agencies and more. While the stakeholder committee has no enforcing power, it plays a critical role in changes regarding the market, tariffs in the NYISO, and other decisions related to the sale and transmission of electricity through the grid. To be approved by the stakeholder committee, any decision requires a 58% approval rate to promote consensus from various sectors and interest groups. From the stakeholder committee, the carbon pricing proposal moves to the NYISO Board for a vote. While the NYISO Board makes the final decision, they look for backing from the stakeholder committee as well as the state; this support is critical for when the proposal moves to FERC for acceptance.

FERC has sole jurisdiction over the NYISO’s decisions and functions, but the NYISO has indicated that they would not file any proposal for approval with FERC without the support of state legislators and the governor. While the NYISO has the mandate to function independently of the state government, in principle the organization aims to function to address the goals laid out by the state. The organization takes its role as an Independent Systems Operator seriously by remaining politically neutral and avoiding taking on a policy advocate role. As a result, determining the social cost of carbon (SCC) that would be used to calculate the carbon price will be determined by the New York Public Service Commission (an agency of the state) rather than the NYISO itself.

WHAT IS THE SOCIAL COST OF CARBON?

The “social cost of carbon” is an estimate of damages in agriculture, public health, energy use, and other aspects of the economy resulting from an additional ton of GHG emissions in the atmosphere, quantifying and monetizing the effects of climate change for use in policy analysis. The largely utilized federal estimate is currently around $50 per metric ton CO2e, which is significantly higher than most existing carbon prices.

New York is one of ten states utilizing the social cost of carbon as a measuring point in energy policies, and NY’s Department of Environmental Conservation and Energy Research and Development Authority are currently developing an official SCC value as called upon by the Climate Leadership and Community Protection Act (CLCPA). This dynamic allows NYISO to draft carbon pricing rules while delegating price-setting to the state to avoid overstepping political boundaries. The federal government’s Interagency Working Group on the Social Cost of Greenhouse Gases (disbanded in 2017) released 2017 estimates for the social cost of CO2 through 2050.

How would a carbon price be implemented?

Internal Emitting Generators

Part 1: Applying the carbon price to bids in the wholesale energy market

The social cost of carbon is expressed as dollars per additional ton of carbon dioxide emissions at a particular point in time, depending on which generating plants are being utilized. Energy suppliers will be subject to this charge based on their carbon emissions, and it will be added to the price that suppliers offer to sell electricity for in the NYISO auction.

For suppliers covered by the Regional Greenhouse Gas Initiative (RGGI) — which currently consists of fossil-fuel-fired electric generating units with a capacity of 25 megawatts or greater— their carbon charge will be determined by the gross social cost of carbon minus the most recent RGGI price. Some power generators, like those supplying low or no-carbon renewable energy, will not be subject to a carbon price.

Part 2: Increasing the energy market clearing prices

Since the carbon charges on suppliers would increase the variable costs of carbon-emitting generation dispatched by the NYISO, a carbon charge would raise the energy market clearing prices whenever carbon-emitting resources are on the margin — where “on the margin” refers to the supplier that provides the last megawatt demanded. So if NYISO needed 20,000 Mwh they might get the first 5,000 Mwh from a wind power generator, the next 10,000 from a nuclear power generator, and the last 5,000 Mwh from a gas power generator. Since the gas power generator provided the last megawatt needed, this supplier would be on the margin and all suppliers, including clean energy resources, would receive the higher energy price, net of any carbon charges due on their own emissions.

Part 3: Providing energy to the consumer

Retail electricity suppliers (Load Serving Entities) would be charged the locational price for power that is demanded, which is a price taking into consideration energy price, congestion cost, and losses (like transportation costs and demand for a specific region). While these retailers would be charged a price that includes the carbon adder, they would also receive a significant subsidy to offset the carbon price. This subsidy would be funded by the carbon charge residual collected from high carbon emissions producers and net imports.

The majority of reports that predicted carbon price impacts worked off of assumptions made before the CLCPA was strengthened to meet more aggressive emissions reductions targets. As a result, predictions on consumers’ costs from these reports are far less reliable. A more recent study by Resources for the Future provides a slightly more accurate prediction, even though it still used assumptions prior to the new CLCPA goals. The study estimated a modest increase in consumer costs at about a one percent increase in consumer costs in the modeled year (2025). Additionally, the report estimates a positive impact on societal welfare in the range of about $118 million to $755 million a year.

External Transactions

If a carbon price is implemented in New York, internal suppliers will face competition from external suppliers who are not subject to the same carbon price, hence increasing imports of energy from potentially high emissions suppliers. This will not only hurt New York suppliers, but it will also undermine the environmental goals of implementing a carbon price. To equalize the market, NYISO proposes a carbon charge to external transactions (imports) equal to a charge that would equalize internal and external transactions. In-state energy suppliers that were exporting outside of New York, exports would buy energy at the locational based marginal price without the carbon effect. While this solution will not incentivize cost-effective carbon abatement outside of New York, it does allow internal and external suppliers to compete in an equal market.

Achieving Carbon Emissions Reduction Goals

Analysis of the carbon pricing proposal has found that a carbon price will help the state of New York achieve its clean energy goals as established by the CLCPA at lower costs to consumers, and will also help grow investment and promote innovation in clean energy, ultimately improving public health. The Brattle Group Analysis estimates that a carbon price would reduce emissions by 2.6 million tons per year, which is 8% of total yearly emissions. It will also provide efficient market incentives for the addition of transmission investments to give downstate New Yorkers better access to valuable low-carbon and renewable resources located in upstate regions. In addition this price will provide incentives for energy producers to update underperforming generating units to more efficient units or replace them with low and zero emissions units.

How does NYISO interact with other bodies in terms of carbon pricing?

NYISO receives substantial input from Carbon Free New York, a coalition of environmental, clean energy, and labor groups who are calling on the NY Forward Advisory Board to consider NYISO’s carbon pricing plan as a tool specifically for economic recovery from the COVID-19 pandemic. It includes the Alliance for Clean Energy New York, New York League of Conservation Voters, and Citizens Climate Lobby of New York.

FERC is the regulatory body with the oversight power to decide whether to approve NYISO’s carbon pricing policy proposal, as any tariff filings are submitted directly from the NYISO Board of Directors to FERC for approval. Currently both the Chairman and Commissioner claim the NYISO does not have the power to mitigate greenhouse gas emissions as they relate to natural gas infrastructure projects. New York’s recently authorized Climate Action Council will be required to give approval for any policy proposed by NYISO before submission to FERC, adding to the complexity of the approval and implementation process for carbon pricing through NYISO.

The NY Public Service Commission has limited financial oversight of NYISO proceedings, but no state agency can dictate actions taken by the NYISO other than by exerting political pressures. The relationship between NYISO, the state government, and FERC has been described as a “jurisdictional battle.” NYISO actively avoids taking any stance on public policy initiatives — it operates within and frames proposals around the framing of both RGGI and CLCPA, aiming to harmonize with state policies as well as federal tariffs while remaining an independent body.

PJM Interconnection

Throughout 2020, the Carbon Pricing Senior Task Force (CPSTF) has been conducting a carbon pricing study authorized by its parent organization, PJM, an ISO that serves more than 65 million people in the Mid-Atlantic region and beyond. Though PJM has been adamant that it is “not proposing to establish a carbon price or policy”, this study is nonetheless crucial if carbon pricing is to be implemented in the future. As per its founding guidelines, the CPSTF is operating in two phases: first, conducting said study to determine the impacts of different carbon pricing scenarios on PJM’s area of operations, and second, outlining the regulatory reforms necessary to implement a particular carbon pricing scenario. Modelling the consequences of carbon pricing is further complicated by the need to account for interactions with RGGI, leakage, and border adjustments. So far, the study infers that PJM-wide emissions would reduce in the event of a carbon price that is implemented only in RGGI states*, a positive sign for climate advocates. However, final authoritative results are still required to determine whether carbon pricing has a future in the PJM region.

*Delaware, Maryland, and New Jersey are current RGGI and PJM members. Virginia and Pennsylvania, both a part of PJM, have committed to joining RGGI shortly.

ISO New England (ISO-NE)

Through its 2020 Regional Electricity Outlook, ISO-NE emphatically advocates for implementing carbon pricing at the wholesale level. With fossil fuels exiting and renewable sources entering New England’s electricity resource mix, carbon pricing can accelerate this substitution in order to fulfill the region’s energy-related legislative mandates and aspirational goals. ISO-NE’s President and CEO Gordon van Welie has publicly advocated for further consideration of carbon pricing, believing it could reduce the timeframe for a clean-energy future. ISO-NE believes that “Pricing carbon within the competitive market structure is the simplest, easiest, and most efficient way to rapidly reduce GHG emissions in the electricity sector.” It also indicates that it is ready to introduce a carbon price at the wholesale level, but lacks the necessary support from New England states and/or federal legislation for this to be actualized.

What challenges do ISOs face when implementing carbon pricing?

Leakage - NYISO

A possible problem with setting a higher carbon price in New York is leakage of high emission energy outside of the state to states with lower carbon prices, and the flow of low to zero-emission energy from out of state energy providers. Exports of high emissions out of the state will negate the progress being made to lower New York state’s emissions and improve public health. Additionally, leakage into the state will disadvantage in-state providers which are competing for bids.

There are certain market design options that can prevent in-state energy producers from facing a disadvantage due to leakage to and from neighboring markets. One option is to charge a fee for importers’ estimated emissions rates to place them on the equal playing field with in-state producers. Another option is to credit (New York) exporters for the energy they send out of the state which reduces emissions in neighboring states. Alternatively, the market could charge importers and credit exporters at the marginal emissions rate and carbon charge in the New York market. This would eliminate the carbon charge on New York generation from the perspective of imports and exports. While the third hybrid option would be the simplest to implement, it would not incentivize importers to reduce emissions.

Resource Shuffling - CAISO

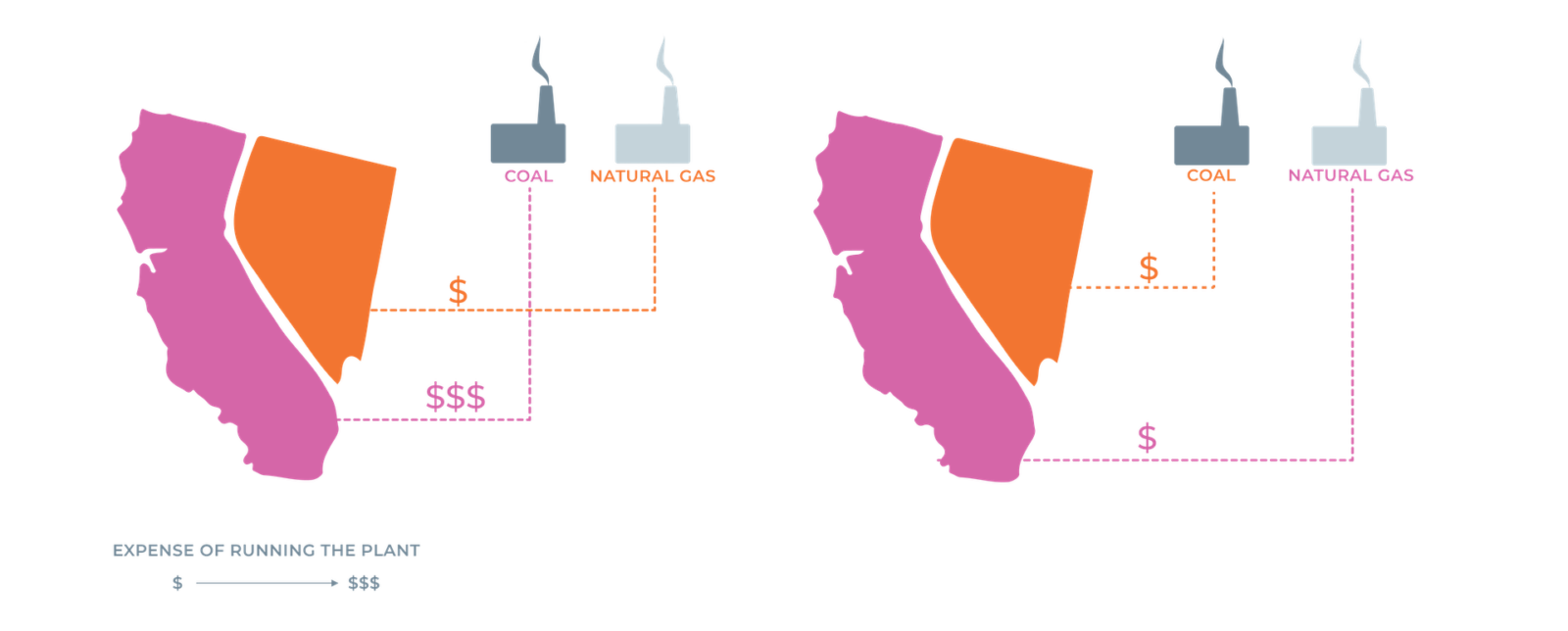

Similarly, California’s ISO is having its own problem leakage, but this time in a different form.

Suppose that two power plants with equal production capacity are both located outside of California’s borders. Plant A burns high-carbon coal, while Plant B uses relatively low-carbon natural gas. For years, Plant A has operated under a contract to sell power to a California utility (for delivery to customers within California’s borders), while Plant B has a contract to sell power to a Nevada utility. Since the California utility must buy permits for its GHG emissions, Plant A becomes more expensive. Shuffling occurs when the Californian utility swaps contracts with the NV utility, thus lowering its compliance costs. Both plants continue operating and producing the same amount of electric power. In this example there is no overall emissions reduction.

However, because both clean and dirty sources in this scenario are outside of California, there is no absolute prohibition or limitation on the operation of the dirtier generating facility. Instead, the dirty electricity may simply be redeployed to serve another location’s demand, resulting in no net reduction in emissions. About 30 percent of the electricity consumed in California is imported from other states. This imported electricity tends to come from disproportionately dirty sources (such as coal) and represents more than half of the carbon dioxide emitted as a result of the state’s electricity demand.

California has attempted to address this resource shuffling problem by adding a carbon price to imported electricity. If the generation source is specified, the purchaser is charged at a rate according to the emissions intensity of that source. The electricity is purchased through the Energy Imbalance Market (EIM), which connects CAISO to surrounding grids in the Western U.S. to exchange electricity in real time.

That said, the generation source of imported electricity is not always specified. In these cases, the purchase is assessed with a carbon emissions intensity similar to that of an efficient natural gas plant, and without tracking the original source of imported electricity, power purchasers are free to “shuffle” their resources. Contracts are then rearranged to replace legacy coal power import contracts with “unspecified” electricity, allowing power purchasers to claim the difference in emissions without making any real changes to the grid.

The impacts of unspecified imports are potentially substantial. For example, in 2016, one-third of imported electricity is unspecified. Had all this electricity originated from coal plants, it would cancel out over half of all claimed electricity sector GHG reductions from 2012 to 2016. The issue cannot be adequately assessed with access to data that EIM has not yet been able to fully monitor. Neither RGGI nor California are set up to monitor the flow of electricity at the level of detail required for such analysis.

Put simply, the future of resource shuffling threatens to undermine California’s environmental goals. About 30 percent of the electricity consumed in California is imported from other states and this imported electricity tends to come from disproportionately dirty sources (such as coal), and represents more than half of the carbon dioxide emitted as a result of the state’s electricity demand.

Recent case law would seem to favor California’s efforts to regulate emissions from out-of-state sources. California regulators operate under a statutory obligation to minimize the leakage associated with the state’s GHG emissions programs, so reducing or eliminating shuffling appears to be required under state law. This is then supported by Califorina’s initial response to the problem of prohibiting it in its initial regulations implementing its GHG cap-and-trade program. Under the first-deliverer approach, California’s cap-and-trade regulations apply to all first deliverers of electricity into the California grid, which includes both electricity-generating facilities in California and “electricity importers.

The outlook of the California carbon-pricing mechanism as a whole?

According to a 2018 CXC report, changes in imported electricity, a direct casualty of the state’s early response to resource shuffling, appear to be responsible for 68% of emissions reductions, as opposed to 32% from in-state generation. While these initially do show an overall decrease in carbon emissions, the full extent to which these reductions are legitimate is unclear. Most reports suggest that given the uncertainty of where nearly a third of CA’s imported electricity is coming from, it is impossible to determine the effect such imports have on their emissions and on emissions in the U.S. as a whole.

The California system of placing a carbon price is still in its infancy and in light of its resource shuffling problem, it is still too early to concretely determine the quality of California’s system. The state’s early findings, however, support a cautious “yes” to the question of whether or not the system is working well enough to continue.

What’s next for ISOs?

Grid Modernization

Recent technological advances have the potential to completely transform the grid, which could impact the work and future of ISOs. The proliferation of renewable energy sources will require a different approach from ISOs, as they must prepare for increased variability in electricity supply (due to their dependence on the weather, such as with sunlight or with wind). Regulatory actions may be necessary to even the playing field for small-scale renewable energy entrants, as they will compete with powerful and expansive fossil fuel producers. The increased prevalence of distributed energy resources (DERs), which generate or store energy closer to the final consumer, may reduce wholesale electricity demand. This could induce dramatic price, supply, and demand consequences for ISO-operated markets, where practices like net-metering might need to be accounted for in the wholesale electricity markets. Other advanced digital infrastructure could automate ISO operations, resulting in labour, capital, and strategy impacts. Such technologies will not just overhaul electricity regulations, but could shape a new energy infrastructure – one that is perhaps less reliant on ISOs and wholesale electricity generators, as consumers increasingly opt for more decentralized electricity possibilities.

For a deeper look at grid modernization, check out this 2020 CXC article: Why Grid Modernization Promises a Stronger Electrical, Environmental and Economic Future

Changing Political Conditions

It remains to be seen how ISOs react to the changing political conditions around them, especially with the 2020 elections looming closer than ever. A Biden presidency will appoint a new Secretary of Energy and other associated staff, promising an enhanced climate mitigation strategy that does not ignore FERC and the ISOs. A second term under Trump may continue the rollback of EPA regulations, with further implications for the electricity grid. Changes in the composition of Congress, as well as 86 state legislative chambers, may further influence the political winds swaying the decisions and abilities of ISOs. The recently published report from the House Select Committee on the Climate Crisis highlights possible congressional priorities on ISOs: improving governance, transparency, and design of ISO-operated markets, promoting state-level clean energy leadership, and requiring FERC to reject energy rates that do not incorporate the cost of greenhouse gas emissions. Political leadership is key to determining the fate of major climate policy initiatives; the results of the 2020 elections could have significant consequences for carbon pricing at ISOs.

For a deeper look at the House Select Committee on the Climate Crisis, check out this 2020 CXC article: House Climate Agenda is a Glimpse at How Democrats Hope to Tackle Climate Change

For a deeper look at the Biden climate plan, check out this 2020 CXC article: Biden’s Clean Energy Plan proposes economic recovery through green investments

Further reading and resources

- FERC – Energy Primer: A Handbook for Energy Market Basics (2020)

- Vox – Clean energy technologies threaten to overwhelm the grid. Here’s how it can adapt. (2019)

- RAP – Electricity Regulation In the US: A Guide (2016)

- DOE – United States Electric Industry Primer (2015)

- Sierra Club – Resource Shuffling in California Graphic